Crypto Fundraising Report H1 2022

The Fundraising Spotlight series is a weekly series by the Coin98 Insight team. However, this will be a special article in the series that delivers insights about the fundraising market in the first half of 2022.

In the past six months, 1,120 fundraising announcements were published, with more than $28.8 billion in value of investments. More logical insights and summaries will be delivered in this article. The source of data in this report is from Dovemetrics and the Coin98 Insights team collected on our own.

Some main insights about the fundraising market in H1 2022 are:

- 1,120 fundraising announcements.

- $28.8 billion in value of investments.

- Ecosystems are deploying less incentive packages to bootstrap project.

- The least attractive category is DeFi, which was the hottest category last year.

- GameFi, NFT & Metaverse received lots of early-stage investments.

- Along with the price of $BTC, the total value of fundraisings witnessed a decline in recent months.

- The total fundraising amount and number of deals in H1 2022 is about 30% higher than that of H2 2021.

Overview of the fundraising market in H1 2022

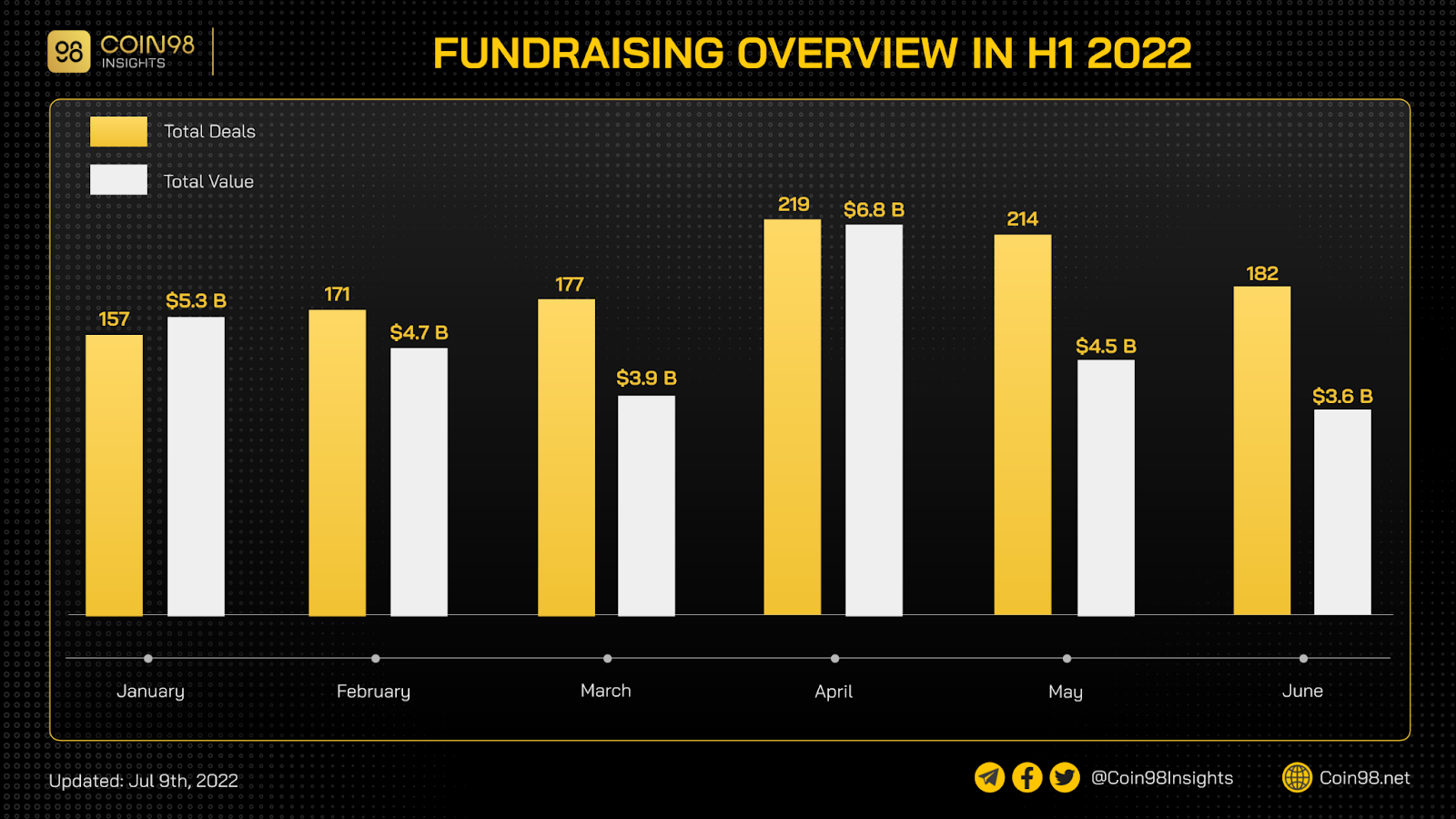

In H1 2022, 1,120 funding announcements were published, thus the average number of fundraising rounds per month is 186. This number increased respectively from January to April, and peaked at 219 in April. In May and June, that number witnessed a gradual decrease.

The fundraising value chart shows the same trend in the last 3 months in H1, 2022. The value peaked in April with $6.8B raised, followed by January with $5.3 billion. The trend shows that the fundraising amount per month is decreasing, which is correlated with the price of BTC and the total value of the crypto market.

In general, while the number of fundings per month was growing, the value was slowly decreasing ($3.6B in June). This shows the correlation between the BTC price and the stream of fundraising inflow in the market. However, the number of fundraisings in H1 2022 still doubles that of H1 2021 (615), and the value of fundraising nearly triples that in H1 2022 ($11B).

Fundraising market in H1 2022 by ecosystem

Incentives program of ecosystems

In H1 2022, the number of ecosystem incentive programs to incentivize builders and users is smaller than that in H2 2021. However, numbers are still impressive.

To compare numbers between H2 2021 and H1 2022:

- There are 16 packages in H2 2021, while there are 14 in H1 2022;

- $9.6 billion is spent on H2 2021, while only $4.1 billion is spent on H1 2022;

- The two biggest is the $750-million packages of Kava and the $725-million packages of Flow;

- In March, the number of announced packages is the highest: 5 packages (Kava, Avalanche, IoTeX, Acala, Fantom). This is the third packages of Avalanche to bootstrap their ecosystem;

- After peaking in March, the number and the value of packages are both dropping sharply. Reason for this trend is mainly the “bear” market, thus incentivizing builders and users at this time is inefficient.

In conclusion, in H1 2022, the “ecosystem incentive packages” trend is no longer at its hottest time. However, the total amount of money spent on those activities was still impressive, and it is witnessing the monthly decline. For anticipation, in H2 2022, there will be much less packages granted by ecosystem foundation, as the efficiency for them is not high enough.

Fundraising market in H1 2022 by sector

Investments in CeFi

In H1 2022, there were 164 investments in CeFi or related to the CeFi category, with a total value of $8.6 billion. There is 1 investment that is worth more than $1 billion, and 25 investments which value higher than $100 billion.

The biggest fundings respectively are Citadel Securities ($1.15 billion), Robinhood ($600 million), Fireblock ($550 million), Circle ($400 million), FTX and FTX US ($400 million each). All of those fundraisings are in late round (from Series A) or Post-IPO.

Both the number and the value of fundraising in CeFi category witnessed complicated trend in H1 2022. Although the number of deals is slightly increasing, the value of them in the last 5 months is much lower than the first.

To conclude, the number of fundraising projects in CeFi category was rising, and the value of them was also increasing. The number of big deals (worth more than $100 million) was also raising in the later months of H1 2022. Accounting for nearly 30% of the total fundraising amount, CeFi was a category that receives lots of attention from VCs and big investors.

Investments in DeFi

In H1 2022, DeFi category fundraising total value was $2.4 billion dollar, with 229 investments, which accounted for 9% and 20% of the total number of fundraising market respectively. The first conclusion is that, among 4 big categories, DeFi was receiving less attention and money than other, as only under 10% of fundraising value was for this category.

Most of the deals was small one, as only four deals worths more than $100 million (Lithosphere Network, Unizen, Capricorn and Rain), and 46/229 deals worths more than $10 million. In compare to H2 2022, the money inflow in this category is much smaller.

While the number of fundraising in DeFi in H1 2022 slightly decreased over the period, the value of them growed significantly. However, in May and June, there are some big investments that raised the monthly value, which explained for the upwarding trend.

In conclusion, DeFi is receiving less attention and money from Venture Capitals and big investors. The average size in DeFi category is $10 million, which is much lower than that of the general market (about $25 million) and that of CeFi (about $50 million).

Investments in blockchain layer-1, layer-2 and other infrastructures

In H1 2022, this category had the total fundraising value of $11 billion (40% of total market value), and had the total number of deals of 276 (25% of total deals). In compared to other categories, this sector had much more attention and inflow of money from big investors and VCs.

33 deals out of 276 were larger than $100 million, 52 deals were larger than $50 million and 131 deals were bigger than $10 million. Some familiar names that raised more than $100 million were Near Protocol, Aptos, Luna Guard Foundation, Optimism, Phantom, Starkware, LayerZero,...

The number and the value of fundraising in H1 2022 in this sector was showing the same trend. They were all among the highest in Feb - Mar- Apr period, showing that in that three months, the inflow of money in this category was the strongest.

To sum up this sector, Layer 1/ Layer 2/ Infrastructure is a huge category and they are attracting VCs and big investors. By accounting for 40% of total fundraising value in the first six months of 2022, this definitely is a sector that should pay attention to in H2 2022.

Investments in GameFi, NFT and Metaverse

In H1 2022, the number of deals in this category was 309 (27% of total deals), while the value of those fundraisings was $5.4 billion (20% of total market value). In compared to other categories, this sector received more attention from big investors and VCs than DeFi sector, but less than blockchain/infrastructure category.

However, this is a new sector that just being paid attention to from the raise of Axie Infinity. Therefore, although the number of deal was high, there were only a few big deals in this sector: 8 deals for Epic Games, OpenSea, Immutable, Sky Marvis, Rario, Punk Comics and Pixel Vault. 77 out of 309 deals worthed more than $10 million, 185 out of 309 deals were seed round investment, and 32 deals were Series A investment.

The number of monthly deal in this category fluctuated in H1 2022. April was the month with the highest number fundings and the highest value of deals. However, in that month, Epic Games only accounted for $2 billion in total value, which explain for the sudden surge of that data.

In conclusion, this is a new sector which only receive lots of traction for under a year. Therefore, most of the deals were low-value, in early round (before Series A). While the number for this sector peaked in April, it was declining gradually because of the unfavorable condition of market.

Fundraising market in H1 2022 for funds

VCs and funds also raised money to expand their investment opportunities and bankrolls. In H1 2022, the fundraising market of funds was also very active. Only 27 deals for funds in H1 2022, but the total value was over $14 billion, thus the average raise of VCs was $500 million.

Some biggest raise were from a16z, Haun Ventures, J◎e McCann, Pantera Capital, Electric Capital, which all worth more than 1 billion. Another insight is that most of the raise was in March and April, as 20/27 deals are announced in this period.

Some medium deals which were worth between $500 million and $1 billion are Sequoia Capital, Hack VC, Dragonfly Capital and Binance Labs. From $100 million to $500 million, there were 13 funds, namely Castle Island Ventures, Amber Group, AngelList, Spartan Group, Fabric Ventures, Framework Ventures, KuCoin Ventures & Windvane,...

To conclude, by raising for VCs, the inflow of money is indirectly increasing in the market, thus developing the crypto market in general.

H1 2022 in general and H2 2022 anticipation

In H1 2022, by looking at the collected and analyzed data, the number is showing that the inflow of money in the market was gradually decreasing in comparison to the inflow of H2 2021.

To compare to H2 2021 data, there were only 842 deals with total value of $22.6 billion. In this half of the year, the focus of funds were blockchain/infrastructure projects, CeFi, and start to raise more fund in early stages for GameFi & NFTs projects.

In terms of VCs, the average size of VCs funding was $500 million which is much higher than the last half of 2021. More and more VCs were raising fund to invest more in the crypto market, thus showing a sign that the money was constantly pouring in the crypto market.

In the second half of 2022, there were some main expectations based on current condition of the market:

- Total fundraising number of deals and value of them will decline in the next 6 months, due to market condition.

- CeFi, blockchain & infrastructure category will continue to receive lots of attention from investors.

- DeFi sector will decline in funding numbers, GameFi and NFTs new projects could still attract early investors to invest in early stages of the project.

- Ecosystems would be less likely to deploy incentive package to incentivize builders and users, as the effectiveness of those activities is unlikely to be high.

Conclusion

Fundraising market is a perfect source of information to find the new trend, to find out what big players are investing in. By carefully following the fundraising market, there will be opportunities for investors and builders.

Also available in

Vie