Crypto M&A Report H1 2022

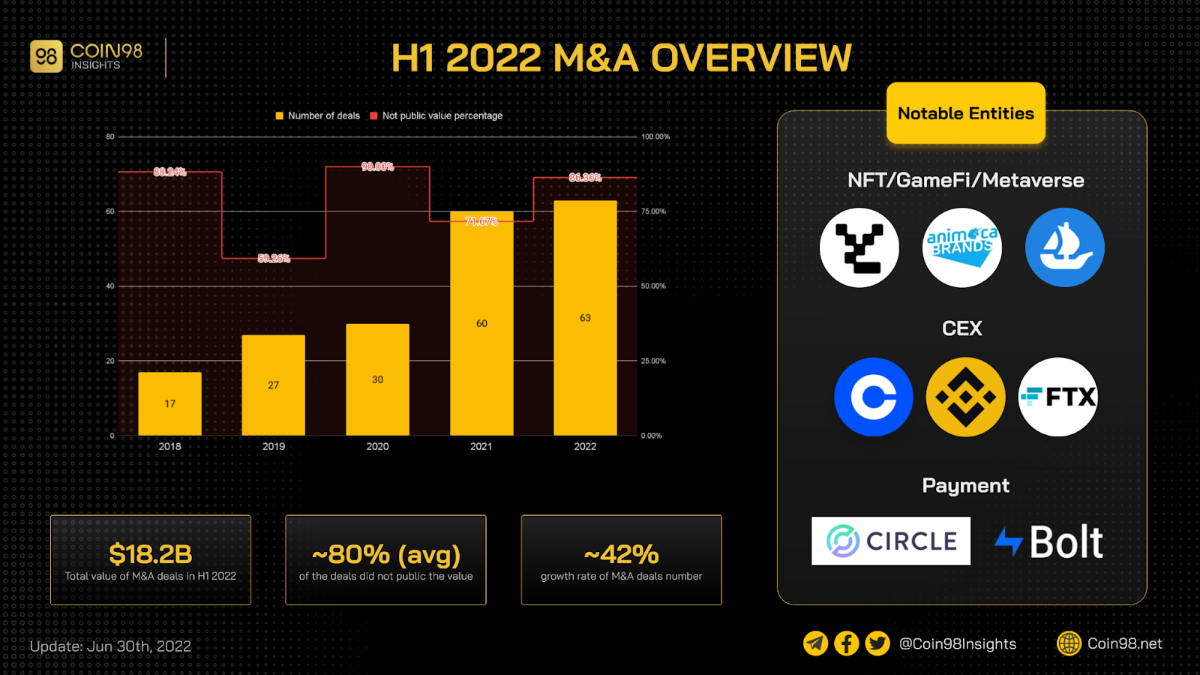

H1 2022 report series is a 6-month series by the Coin98 Insight team. In this report, insights about the M&A market in the first 6 months of 2022 will be presented. By using data from Dovemetrics and some other collected sources, 63 M&As are recorded.

Key Insights:

- 63 M&As are recorded;

- The company that has the most M&As is Animoca with 6 deals in that period, followed by FTX with 4 deals;

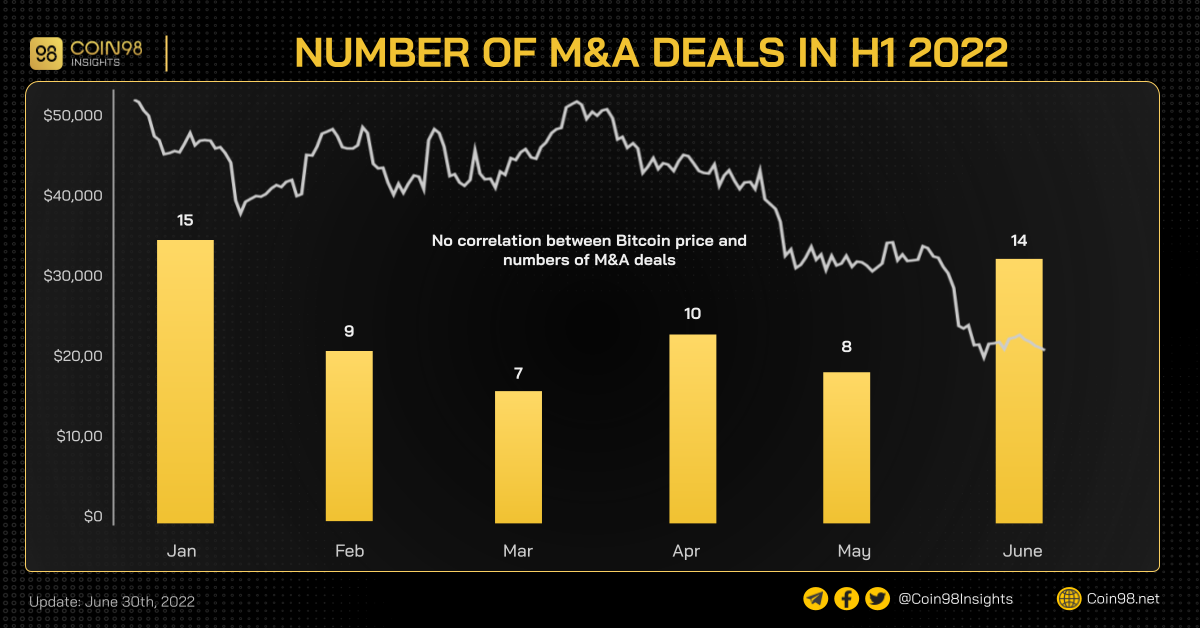

- January is the month with the most M&A transactions announced (15 deals);

- The amount of recorded M&A in H1 2022 is 50% higher than that in H2 2021, and nearly doubles that in H1 2021;

- As the value of deals is usually not announced, only $18 billion are recorded on 9 deals that published the deal value.

Overview of Crypto M&A market in H1 2022

In H1 2022, the Crypto M&A market witnessed 63 deals with most of the deal were in CEX, GameFi & NFT categories. Out of 63 deals, there were 11 acquisitions of CEX projects, 14 acquisitions of NFT-related projects, 11 acquisitions of GameFi projects.

The first month of H1 2022 had the highest amount of acquisitions (15), followed by the last month of the same period (9). The average amount of M&A per month in H1 2022 is about 11, which doubles that in 2021 (5).

In general, there is no connection between the number of M&A transactions per month and the price of $BTC in H1 2022.

The total value of M&A deals in the first half of 2022 was recorded at $18.2B (according to Dove Metrics). However, Zynga's acquisition by Take-Two cost $12.7 billion USD (accounting for nearly 70 percent of the total value). Additionally, neither of these two businesses has a strong relationship to or direct influence over the cryptocurrency market.

From 2018 to 2021, there was an average growth rate of 42.04% in terms of quantity. In the first half of 2022 alone, the number of deals is larger than in the whole of 2021.

This demonstrates how institutions' financial potential in the cryptocurrency market is expanding. In addition, it’s also an expansion of adoption because Dove Metrics statistics include parties that have no or little direct influence over crypto market.

CEX and NFT/GameFi are two categories with many notable points. These two categories account for 17.5% and 39.7% of the total number of deals, respectively.

With four deals completed this year, FTX exchange can be considered the most significant project in the CEX segment. With NFT/GameFi category, Animoca and Yuga Labs are sizable companies with prominent deals in the marketplace.

In addition, through M&A deals, we are also aware of the ambitions of organizations:

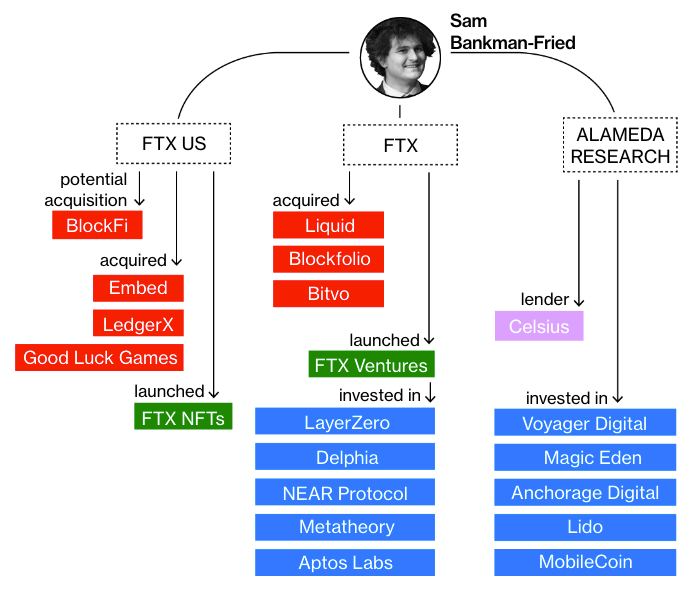

- FTX with its acquisitions after Celsius and Three Arrows Capital dramas shows the goal of acquiring a larger customer base and increasing its reputation.

- Animoca, a large investment fund continues to expand and become the leader in the GameFi/NFT/Metaverse segment.

- Yuga Labs acquired Larva Labs with the intention of becoming the leading NFT/Metaverse builders.

Details of each sector will be analyzed in-depth below.

Crypto M&A in H1 2022 in the CEX category

In M&A market, deals will often be done by centralized exchanges. Due to their substantial financial resources and traditional business models, this group of companies frequently engages in corporate acquisitions.

In H1 2022, there are 11 M&A deals in CEX category: most of them are from top CEXs in the market such as FTX, Blockchain.com, Gemini, Coinbase,...

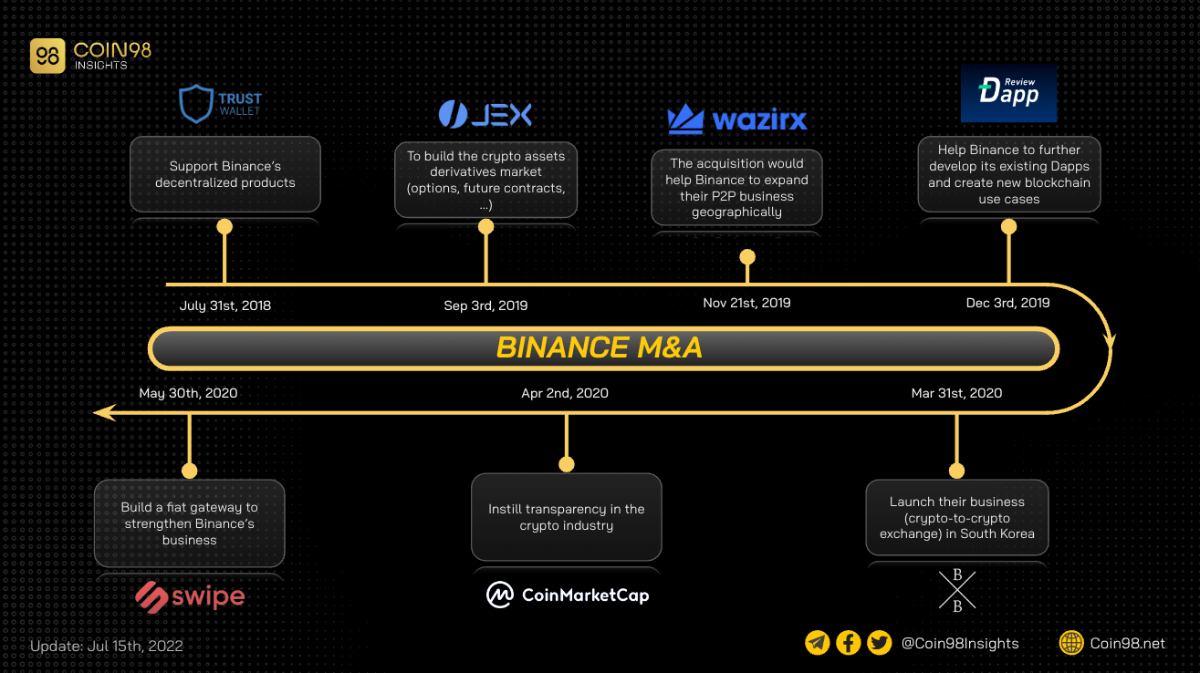

Binance

Binance did not carry out any M&A deals in the first half of 2022. Prior to then, they completed 7 M&A deals with well-known companies such as Trust Wallet, WazirX, Coinmarketcap, Swipe.io,...

These deals were all done at a time when the market was not active, and BTC prices went sideways in a low area.

This indicates that:

- Binance took advantage of the motionless market to buy companies at attractive valuations.

- Binance is also a company that has the ability to manage cash flow effectively, so they can carry out M&A deals with great value.

- In addition to developing centralized products, Binance is also very interested in the transparency of the crypto market, they have made numerous acquisitions of data companies or non-custodial wallets.

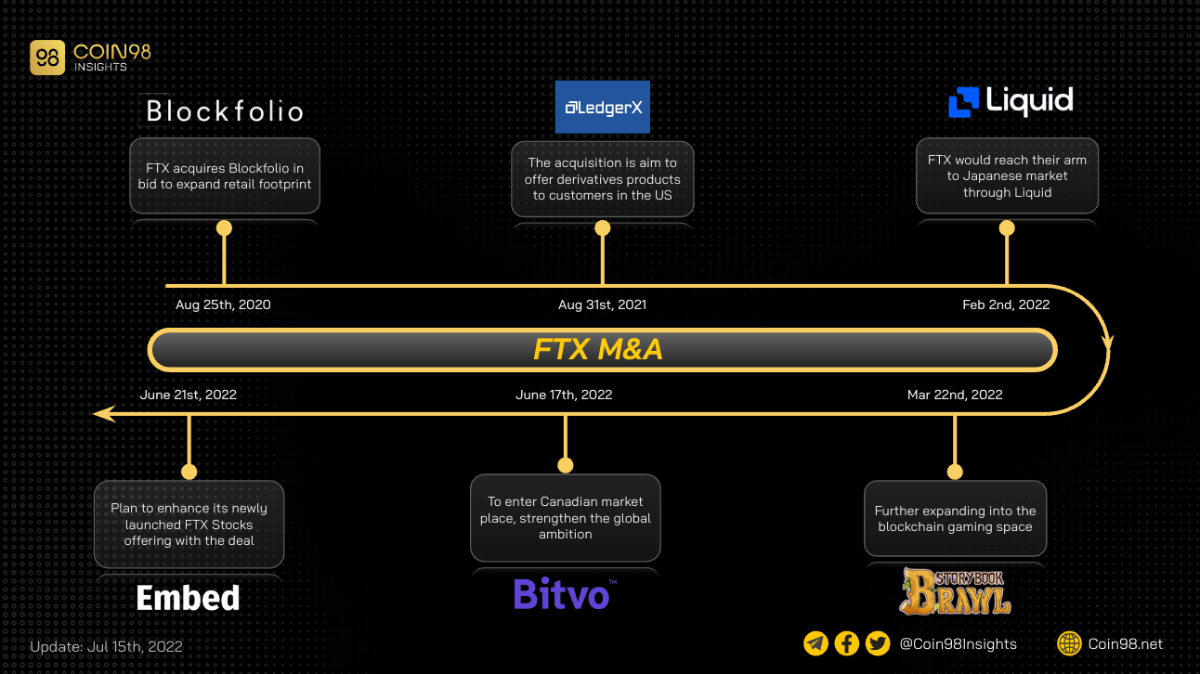

FTX

3 projects are acquired by FTX (Embed Financial, Bitvo, Liquid Global):

- Embed Financial: A company to enhance stocks trading offering for FTX US.

- Bitvo: Canadian crypto trading platform to enter the Canadian marketplace.

- Liquid Group and all of its operating subsidiaries: Including Quoine Corporation - one of the first crypto exchanges to be registered by the FSA in Japan.

By acquiring many new CEXs in different areas and different advantages, FTX is expanding to the stock market in US, and crypto market in Canada and Japan. Through those acquisitions, Canada and Japan are two markets that FTX will develop more in the future.

In H1 2022, the number of FTX acquisitions raised suddenly as the valuation of projects was much lower in the bearish market. Both FTX and Binance took advantage of the red market to strengthen their empires.

Besides, FTX is also targeting many companies after Celsius/3AC-related dramas,... some companies such as Voyager, BlockFi,...

Therefore, it is likely that in H2 2022 Sam Bankman-Fried together with FTX will continue to increase the number of acquisitions.

Gemini

Gemini acquires Omniex in January, thus there are totally 4 projects that Gemini acquired.

- Omniex: A trading technology platform that provides order, execution, and portfolio management system solutions for institutional crypto trading.

- Shard X: Increase the speed at which Gemini can transfer customer assets and increase usage of assets on its platform.

- Nifty Gateway: Allows users to purchase NFTs from crypto games using credit and debit cards

- Blockrize: Crypto credit card firm.

As Gemini acquires many new projects and companies, they are expanding its services to serve its customers better by improving its trading technology, and increasing customer accessibility to NFT and crypto assets from credit and debit cards.

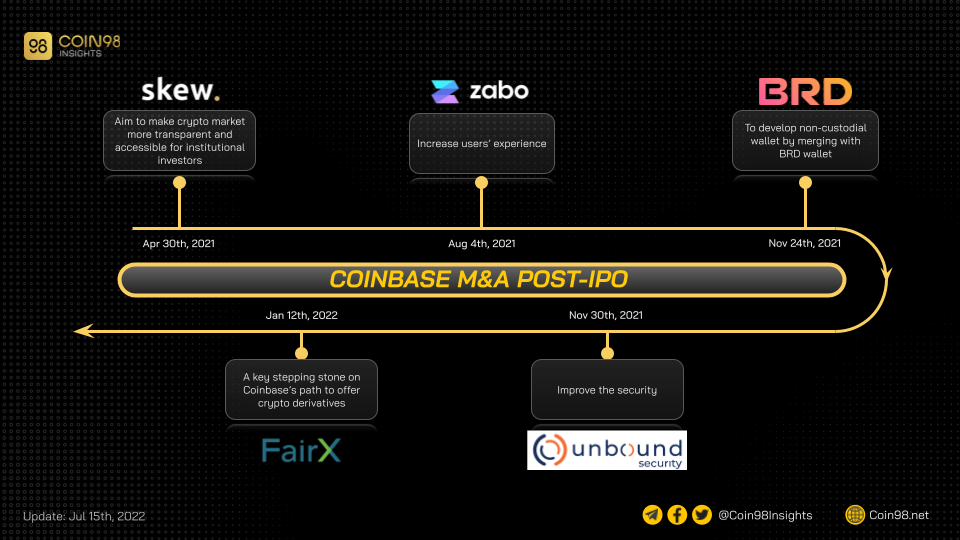

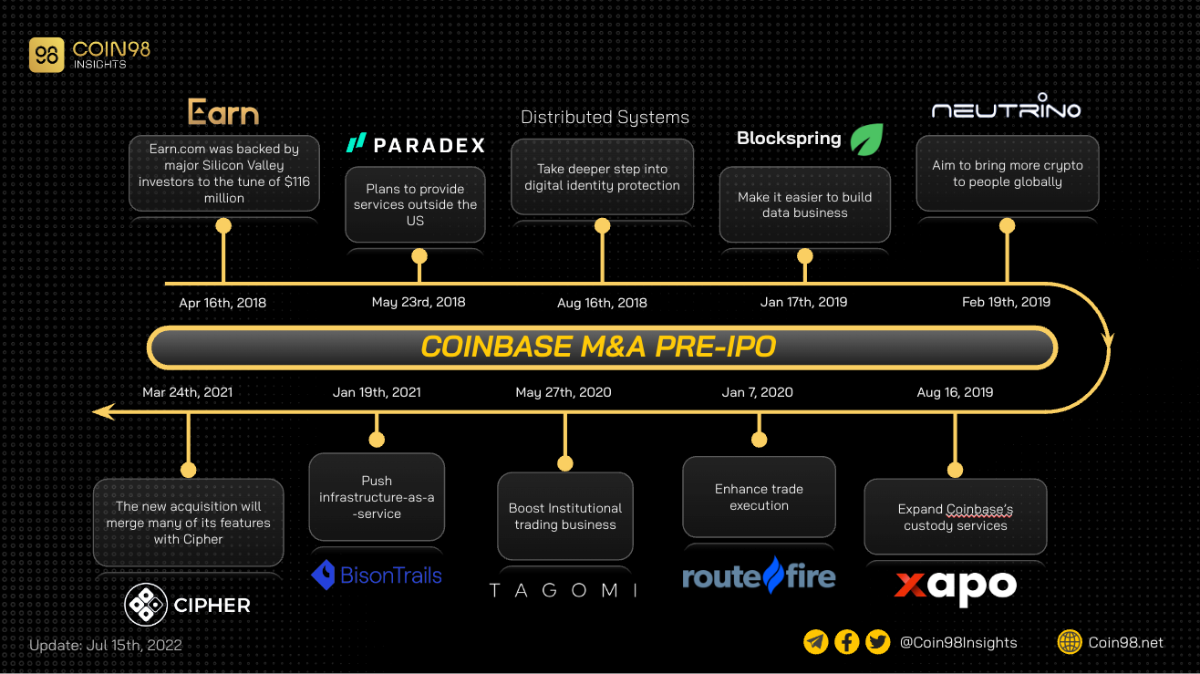

Coinbase

In the first half of 2022, Coinbase only acquired FairX - a CFTC-licensed derivatives exchange, which has raised $ 27.5 million in a Series B round (according to Crunchbase).

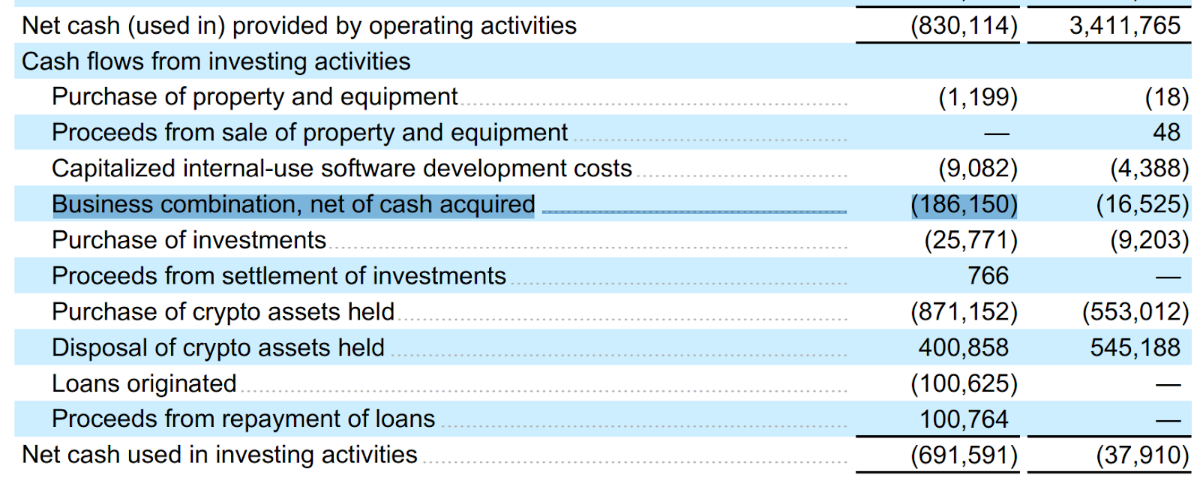

According to the cash flow statement published by Coinbase, the “Business Combination” caused a negative ~186 million USD, so this could be the price for Coinbase to acquire FairX.

This is a step toward Coinbase's goal of competing with FTX US by expanding its business through derivatives.

However, the growth rate in number of Coinbase's M&A deals in 2022 and after the IPO has a sharp decline.

Despite the fact that the financial situation was quite good following the IPO, Coinbase only made 5 M&A deals.

Coinbase announced 10 M&A deals prior to its IPO. Thereby, it is possible to see the "short of breath" or change in the development direction or perspective of Coinbase on mergers and acquisitions.

Crypto M&A in H1 2022 in the GameFi & NFT category

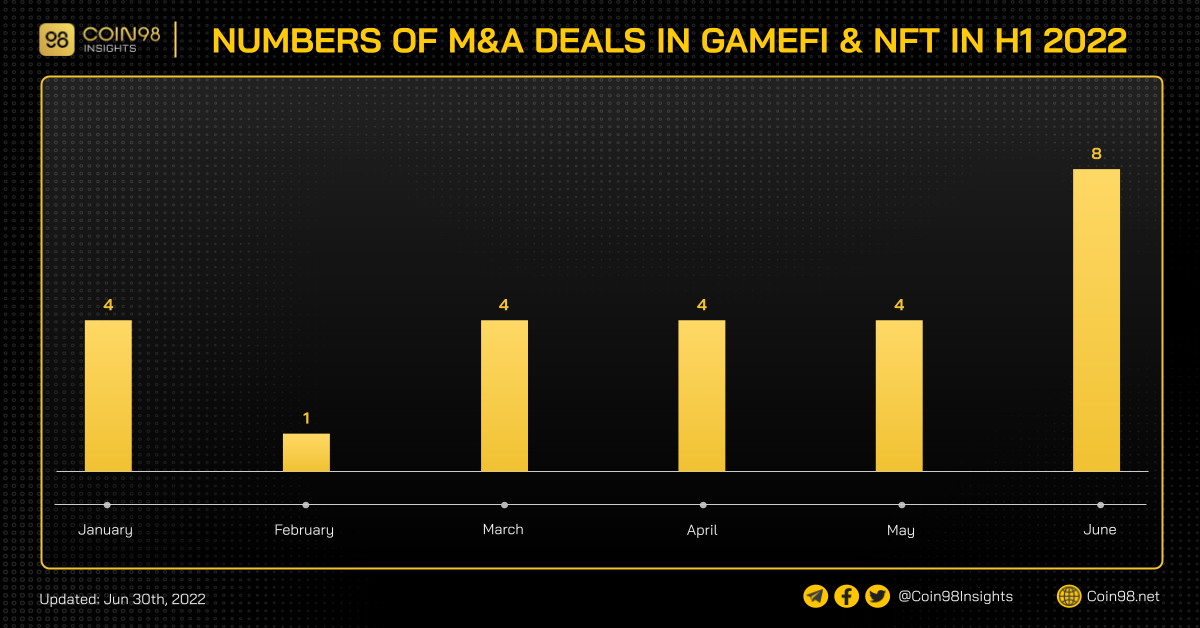

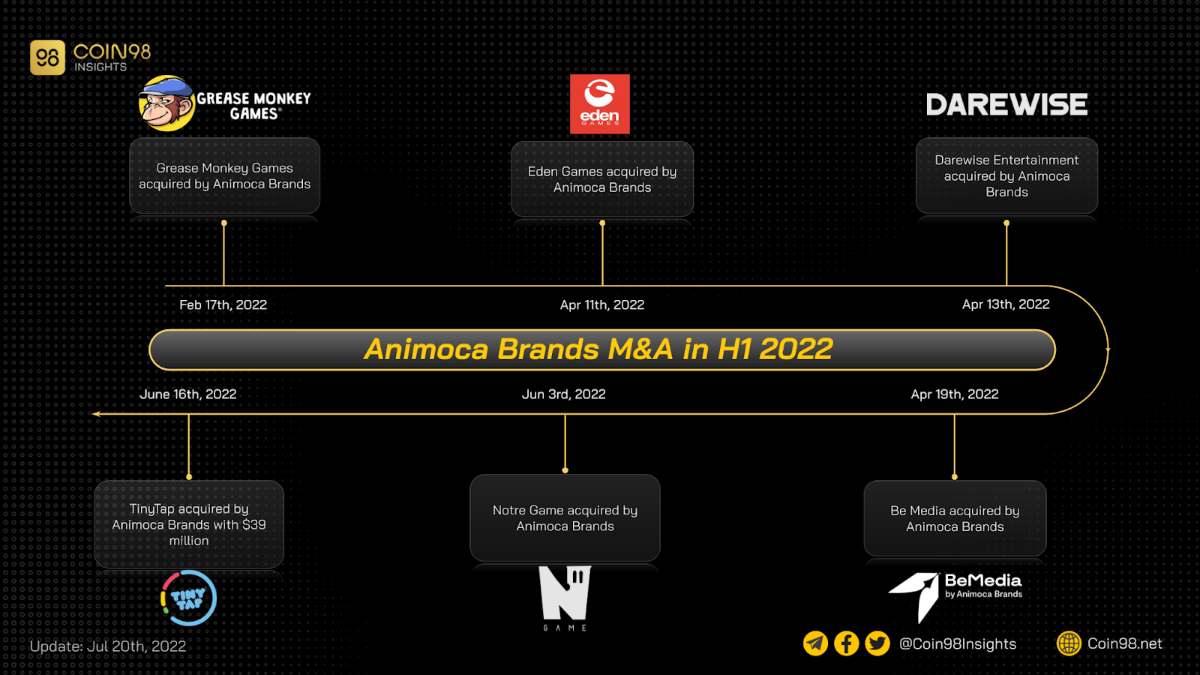

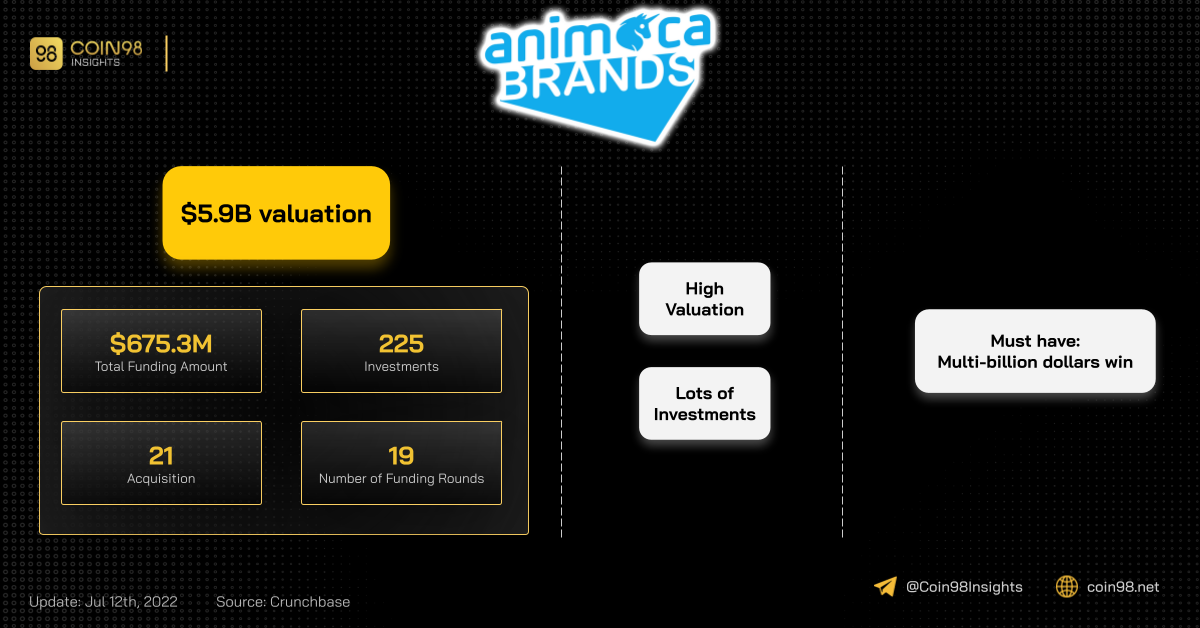

In H1 2022, there are 25 deals in GameFi & NFT category, with the highest amount of deals is from Animoca Brands. In 6 months, they acquired 5 projects, namely TinyTap, Notre Game, Darewise Entertainment, Eden Games, Grease Monkey Games.

The M&A market in this category is constantly growing in H1 2022, as that number peaks in June with 8 deals. Companies and projects are paying more attention to the M&A market, as acquiring a project is a time-saving method for a company to grow.

The number of deals in this category has a reverse connection with the general situation of crypto market. As the market was going “down”, more acquisitions are announced as the valuation of acquired projects are smaller, which favor the real and long-term builders to buy and grow their business.

In the fundraising market, the GameFi & NFT also received special attention (the number of deals in this category was 309 - 27% of total deals, while the value of those fundraising rounds was $5.4 billion - 20% of total market value.

In the following part, big M&As in NFT Marketplace would be analyzed, before mentioning the two biggest acquiring companies in H1 2022.

Significant deals in NFT Marketplace

NFT Marketplace is gaining attention from the market with many acquisitions:

- Uniswap acquired Genie (an NFT marketplace aggregator) to expand its products to include both ERC-20s and NFTs. After this acquisition, users can buy and sell NFTs directly on Uniswap website. This is the first time that a popular DEX as Uniswap acquired an NFT marketplace, which possibly start a new trend for DEX developers.

- KnownOrigin acquired by eBay: This is another popular acquisition in H1 2022. As NFTs are becoming a hot space for creative developers, eBay has joined the field with this acquisition. eBay brand and community is a big support for the development of KnownOrigin and the NFT space in general.

- NFTrade is acquired by BNB Chain: As there was lack of trustful NFT marketplace on BNB Chain, and BNB Chain is a potential ecosystem for developing NFT, GameFi and Metaverse. After this acquisition, NFTrade would be one of the biggest NFT marketplaces in this chain.

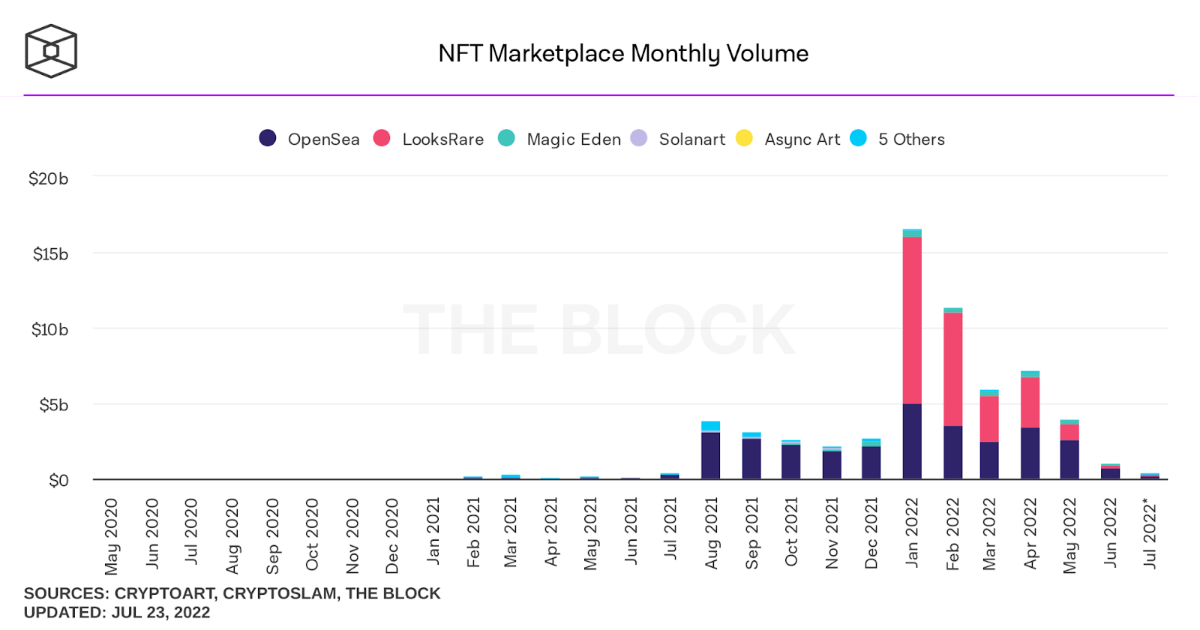

- Opensea acquired Gem and Dharma Labs: This biggest NFT marketplace acquired two smaller projects - an NFT aggregator and an on-ramp project to connect fiat to NFT market.

The volume of NFT transactions on Marketplaces has steadily decreased since the beginning of the year. However, there are still new entrants into the market, such as Uniswap.

When a product is in its early stages, there will often be more fundraising deals and product releases than M&A. The upward trend in M&A for NFT Marketplace indicates a shift in the product's development stage (from growth to maturity).

As a result, the NFT Marketplace is currently experiencing intense competition (in a specific ecosystem), and it is likely that only organizations with significant resources will emerge as winners. These could be seen clearly in the Ethereum and Solana ecosystems and possibly BNB Chain in the near future.

In conclusion, NFT Marketplace is a developing sector in the crypto market, which get lots of attention from both fundraising and M&A market in H1 2022.

Animoca Brands acquisitions

By acquiring many new projects in GameFi & NFT category, Animoca Brands is building their own ecosystem. In projects that they were acquiring:

- TinyTap: Educational technology company that provides a no-code platform enabling educators to create and distribute interactive educational content.

- Notre Game: A game development and publishing company.

- Be Media: Australian digital marketing agency to focus on key opportunities in Australia centered around blockchain development.

- Darewise Entertainment: A game developer founded by veterans of the AAA games industry that is currently developing the high-quality blockchain MMO Life Beyond, and developed Assassin’s Creed IV: Black Flag, Assassin’s Creed Unity, Dying Light 2, Black & White, Tom Clancy's The Division, and the Fable series.

- Eden Games: Developer of Need for Speed: Porsche Unleashed, F1® Mobile Racing, Gear.Club, and Test Drive.

Animoca Brands is acquiring top game developers behind top games Assassin’s Creed IV: Black Flag, Assassin’s Creed Unity, Need for Speed,... There is an anticipation that Animoca Brands is building their own ecosystem around gaming products, with top developers to deliver top GameFi projects to crypto market in the future.

After a recent $75 million dollar funding round, Animoca Brands has been valued at $5.9 billion. With the above valuation, Animoca Brands' portfolio is required to have from one to a few big winning investments (exit at multi-billion dollar valuation).

As a result, Animoca Brands will be the builder we need to pay attention in the next Bull market.

Gaming is a traditional market, therefore the acquisition of a crypto-oriented VC (venture capital) to game developing companies marks the combination between both markets. As one of the biggest VCs who is investing in the GameFi category, Animoca Brands is leading the development of this sector.

Yuga Labs acquisitions

However, the value of the deal is not publicly disclosed. This deal is the pioneer in the NFT sector that announced an airdrop after an acquisition, therefore starting a new wave of NFT project that generate their fungible tokens to bootstrap NFT value.

One of the hottest acquisitions in H1 2022 in NFT sector is the acquisition of Yuga Labs to CryptoPunks and Meebits, before announcing the airdrop to give commercial rights to the community (March 12th, 2022).

Yuga has acquired the IP of the CryptoPunks and Meebits NFT collections from Larva Labs, including the brands, the copyright in the art, and other IP rights for both collections, along with 423 CryptoPunks and 1711 Meebits.

Crypto M&A in H1 2022 in other categories

In terms of other categories:

- 3 DeFi deals in January and February: Tap Finance acquired by PsyOptions, Avari acquired by Maple, Votemak acquired by [REDACTED] Cartel.

- 6 infrastructure deals: Spreading from January to June, many infrastructure projects are acquired by Circle (the company behind $USDC), Nansen, Chart Prime, Kaiko, Namecheap and NCR Corporation.

- 5 deals in the asset management category: As most of the companies and projects in this sector are traditional finance market who is expanding to crypto, there is no familiar name in this sector. Most of the acquisitions are from asset-management companies who want to explore more profitable assets in crypto market to provide their users with new choices.

- 5 projects in the payment and on-ramp category: This sector is the gateway to crypto market for investors in many regulated countries. The acquiring company in this sector were Bolt, Blockdaemon, Fireblocks, Elrond Foundation, with unknown value of the deals.

Payment

Payment and On-ramp is an important category in the market, as it is the gateway for traditional users to access crypto market. Therefore, the development of this sector could be a good sign for crypto mass adoption.

There are 5 deals in the payment and on-ramp:

- Circle acquired Cybavo - a digital asset infrastructure platform that focuses on custody and blockchain application development.

- Blockdaemon (infrastructure platform) acquired crypto on-ramp company Gem. Gem offered trade data aggregation service and a know-your-customer (KYC) product.

- Utrust was acquired by Elrond Foundation: By acquiring Utrust - a payment project, Elrond planned to take over European crypto payments with exchanges, VISA cards, and banking connectivity that complies with evolving regulations.

- Wyre was acquired by Bolt for $1.5 billion which is the only publicly-announced value of the deal in the payment sector.

- Silvergate acquired Diem payment’s network intellectual property and other assets. The deal would help Diem to present its stablecoin in the crypto space.

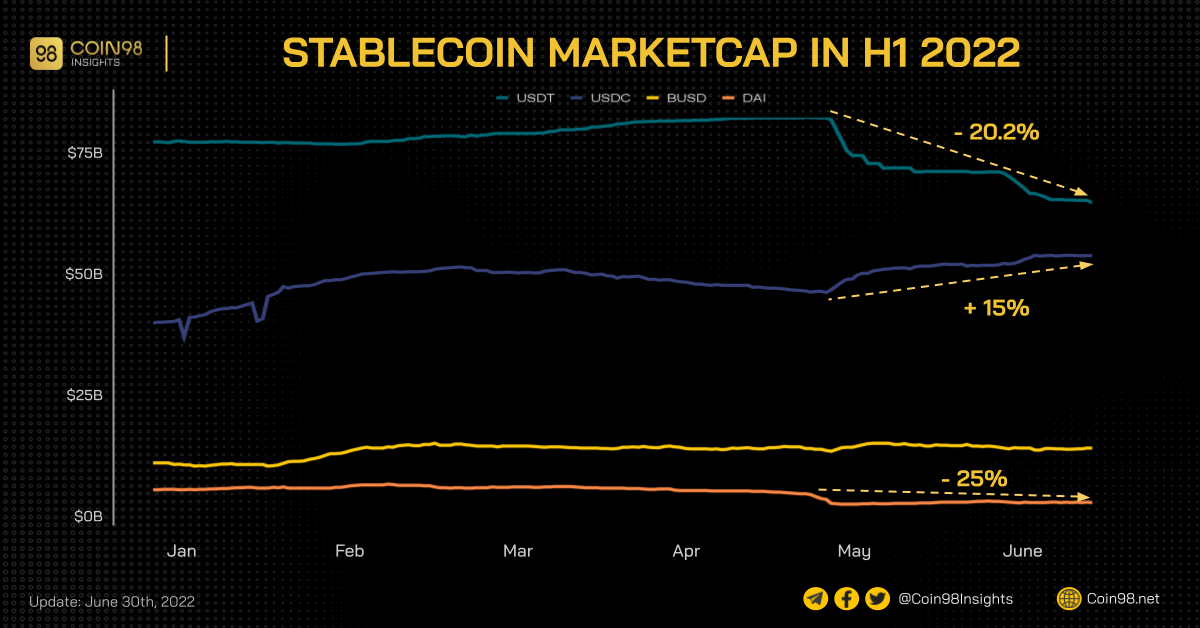

The stablecoin market is one of the essential foundations for the Payment category in the crypto space. However, in 2022, the market capitalization of this market is heavily affected after the Terra event. Other major stablecoins like USDT or DAI all saw a drop in capitalization.

In contrast, USDC (stablecoin issued by Circle) has grown in terms of capitalization. Overall, the entire stablecoin market has still recorded a total capitalization of 8.3% (according to DeFi Llama) since the beginning of the year. This data does not bode well for the growth of crypto payments.

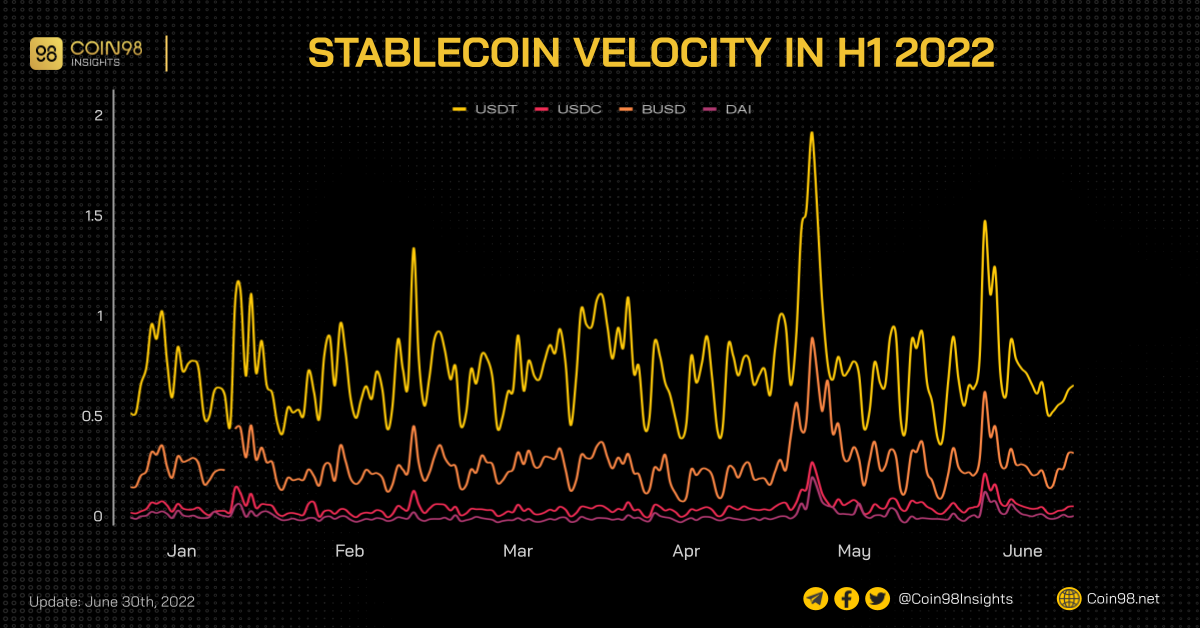

Despite impressive market capitalization growth, the Velocity Index (calculated by Volume/Cap, data from Coinmarketcap) from the beginning of the year to the end of June 2022 shows that USDC is used less than BUSD and USDT in the field of trading crypto.

As a result, in order to truly become the leader in stablecoins sector, Circle will need to expand USDC's use case coverage in both real-world payments and crypto transactions.

In H1 2022, Circle also made an acquisition of Cybavo, a company active in the field of institutional custody. Therefore, this acquisition is unlikely to have a big impact on the growth rate and application of USDC.

Another notable deal in the payment sector was Bolt’s acquisition. The firm has acquired crypto company Wyre in a deal valued at around $1.5 billion.

This is the only deal that publishing their value in the payment sector. After this acquisition, Bolt’s CheckoutOS would be announced — a one-click checkout, authentication, payments, and fraud protection. Before this acquisition, in 2018, bitcoin smart contract developer Hedgy was acquired by Wyre.

Although the number of deals in this sector was still small, the value of deals was high and the acquiring companies were popular names (Circle, Blockdaemon, Elrond Foundation). High-quality deals showed a sign that big players have been paying attention to this sector, and we could expect more big M&A deals in the payment category in the future.

DeFi

According to Dovemetrics, in H1 2022, only 3 M&A in the DeFi is announced, without publishing the valuation.

After many “bearish” events such as the collapse of Terra, Celsius, Three Arrows Capital, the TVL of DeFi witnessed significant drop (from over $200 billion to just over $61 billion - 67% decrease).

As the TVL dropped, the revenue of protocols also decreased. This could be one of the biggest reasons why DeFi M&As accounted for just a small number of the total deals.

On the other hand, M&A for the DeFi has not actually been applied too much even during the period when they have the strongest growth (2020-2021).

Even in the most-developed time of DeFi, the number of DeFi M&A deals was still small. There are also other reasons for this situation.

- First, DeFi protocols usually have small budgets even after fundraising. Therefore, acquiring other projects are hardly achieved.

- Second, in terms of merging projects, merging DAO and technology are extremely complicated, thus only a few DeFi projects were excited with the M&A market.

In detail, in H1 2022:

- PsyOptions - an option protocol on Solana acquired with Tap Finance - a small project in DOVs sector. However, the option sector didn’t receive much attention from users until now.

- The acquisition of Votemak from Redacted Cartel is a notable deal in the DeFi sector because of the importance of Redacted Cartel in Curve War. However, this sector is facing lots of challenges since the collapse of the biggest algorithm stablecoin $UST.

- Maple Finance acquired Avari to launch their product on Solana: After launching on Solana for nearly 6 months, the TVL of Maple on Solana is $133 million, which accounted for nearly 10% of the total TVL of Maple ($1.6 billion). As the TVL on both ecosystems was growing fast in the last 6 months, the revenue of project also increased.

In conclusion, DeFi in the M&A market was not a hot sector due to many reasons. After the M&A deals, except for Maple Finance, other projects didn’t show significant changes in terms of revenue and users.

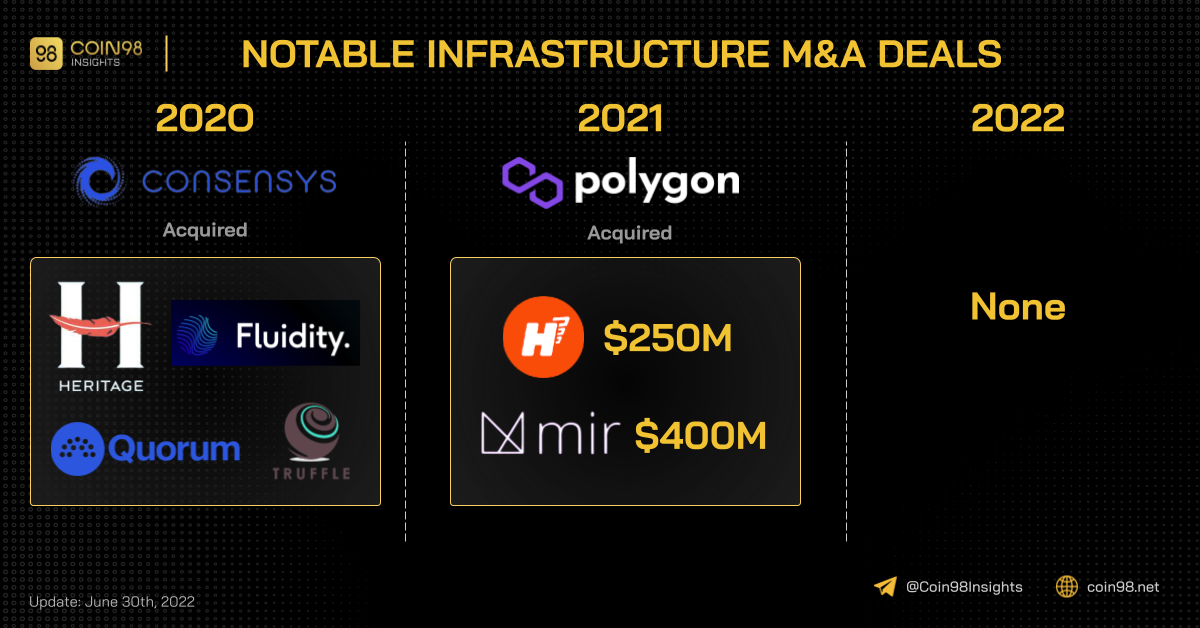

Infrastructure

Not many deals have been done in infrastructure. This sector in H1 2022 has witnessed some deals in terms of data analysis platforms (Nansen, Chart Prime, Kaiko, Quicknode …), Wallet (Consensys), and others.

However, it can also be seen here the importance of information aggregation and transparency even for the crypto market.

In general, in the first half of 2022, there were no outstanding acquisitions of Infrastructure platforms like in the previous period.

Some notable M&A deals in the infrastructure sector in the past:

- Polygon acquired two Zk-Rollups solutions (Hermez and Mir Protocol) in 2021.

- Consensys (builders of Metamask) also made 4 M&A deals in 2020.

When compared to the Fundraising market, Infrastructure has always been the place to receive investment cash flow, even though market sentiment has not been very positive since the beginning of the year.

Therefore, we can draw the conclusion that currently, Infrastructure is still in the process of development, the market is still not yet mature enough and the competition is not too fierce for more M&A deals.

This demonstrates the crypto market's significant growth potential.

Crypto M&A Market H1 2022 in general

In general, the M&A market in the first half of 2022 has the following highlights:

- M&A deals are appearing more frequently with high growth rates. However, due to statistical issues, there may be errors (as many companies/deals have little or no influence on the crypto market are included in the list).

- M&A has done mainly on CeFi companies, there is no sign of merging of DAOs (on-chain execution) becoming mainstream in near future due to technical and governance issues..

- M&A activity is growing in high-competition niches such as CEX and NFT Marketplace.

- As the market collapsed, the valuation of projects would reduce. Therefore, this is a good time for big companies to acquire smaller teams to develop their projects faster. Animoca Brands and FTX were the most active acquiring companies in H1 2022.

- The GameFi & NFT sector attracted lots of money in both M&A and fundraising market. Many gaming studios are acquired by crypto teams to develop the next generation of GameFi, and Animoca Brands is the biggest acquiring team in H1 2022.

In addition, when M&A deals appear with increasing intensity in certain categories, it is very likely that that product/category is approaching the maturity stage.

As a result, retailers are likely to have fewer opportunities to invest in such categories (CEX, NFT Marketplace,…) with a high return on investment.

In the second half of 2022, there were some main projection based on current condition of the market:

- The number of mergers and acquisitions will most likely decrease because the macro situation has a significant impact on companies' financial resources. Furthermore, interest in cryptocurrency appears to be dwindling.

- Crypto-native organizations with strong financial standing continue to grow in control and influence ⇒ There may be acquisitions from familiar names in H2 2022.

- Accordingly, based on the above analysis, FTX, Binance, Animoca Brands, Opeasea, Uniswap, Yuga Labs, ... will be the names we need to pay attention to in the near future.

In general, in compared to the previous years of the crypto market, the M&A market was more active as the number of deals, the value of announced deals and the participants in H1 2022 was all bigger.

Conclusion

Through statistics and analysis of M&A deals, we can see that the M&A trend for crypto companies is more and more popular with the growth in number and value.

CEX and NFT/GameFi are sectors have witnessed impactful merger activities in the first half of 2022 with deals of big players such as FTX, Animoca Brands, Yuga Labs, Opensea, etc.

Besides, the payment sector also has notable deals like Elrond, Circle and Bolt. As for other sectors like DeFi or Infrastructure, there are not many highlights.

Although the crypto market is going through a difficult time, the growth rate of M&A deals has not shown any signs of slowing down. Proving that there are organizations that still possess strong economic resources, these will most likely be the names to watch out for and the foundation of the next season of growth.

Also available in

Vie