Blockchain Explained: What is Blockchain Technology?

What is Blockchain?

Blockchain is a digital ledger of all cryptocurrency transactions. It is constantly growing as "completed" blocks are added to it with a new set of recordings. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data.

The data that is stored on a blockchain is distributed across the network of computers that make up the blockchain. This means that no single entity can control or tamper with the data. This makes blockchain a very secure way of storing data.

Blockchain is often referred to as a Distributed Ledger Technology (DLT). This is because each computer or 'node' in the network has a copy of the ledger. This makes it very difficult for anyone to tamper with the data.

Why do we need Blockchain Technology?

The world is built on trust. We trust that the money in our bank accounts is real and that it will be there when we need it. We trust that our government officials are acting in our best interests. We even trust that the food we buy at the grocery store is safe to eat.

But what happens when that trust is broken? This is where blockchain comes in.

Blockchain has the potential to revolutionize the way we interact with the world around us. By creating a decentralized database, blockchain can help to build a more trustful society in which people no longer have to rely on central authorities to keep their information safe.

In other words, blockchain can help us to create a world in which we can all be our own banks, governments, and grocery stores. And that is why Blockchain Technology is so important. It has the potential to empower individuals and make the world a fairer and more trusting place.

Limitations of traditional transactions

There are several limitations of traditional transactions that prevent them from being used in today's world.

- First, traditional transactions are slow and often take days or even weeks to complete. This is because each step in the process must be completed manually, which can be time-consuming.

- Additionally, traditional transactions are often complicated and require a lot of paperwork. This can make it difficult for people to understand the process and may result in errors.

- Finally, traditional transactions typically involve high fees, which can make them prohibitively expensive for some people.

For these reasons, traditional transactions are often not the best option for people who need to complete a transaction quickly and cheaply. Instead, they may want to consider using alternative methods such as online payments.

Limitations of transactions through the banking system

There are several limitations of transactions through the banking system.

- First, banks typically charge fees for their services. These fees can be quite high, depending on the bank and the type of transaction.

- Second, banks may not be able to process transactions immediately, particularly if the transaction is large or complex. This can cause delays in getting funds to the intended recipient.

- Third, banks may place limits on the amount of money that can be sent through their system at one time. This can be a problem for businesses or individuals who need to send large amounts of money quickly.

- Fourth, information from the banking system can be stolen, which can lead to identity theft and other financial crimes.

- Finally, banks may require that customers have certain account balances in order to use their services, which can exclude some people from using this method of payment.

⇒ Overall, the banking system has some advantages and disadvantages. Therefore, Blockchain Technology has the potential to compete with the banking system by providing a more efficient and secure way to send and receive payments.

Who invented Blockchain?

The person behind the development of Blockchain Technology is Satoshi Nakamoto. However, it is still unclear whether this is a real person or a pseudonym for a group of developers. What we do know is that Nakamoto published a white paper in 2008 which outlined the concept of a decentralized digital ledger. This was then implemented in 2009 as the Bitcoin network.

The creation of Bitcoin and Blockchain Technology was a major breakthrough in the world of finance. For the first time, it was possible to send and receive money without the need for a central authority. This made transactions much faster and more efficient.

Blockchain Technology has since been used for other applications such as smart contracts and supply chain management. It is clear that Nakamoto's invention has had a profound impact on the world and will continue to do so for many years to come.

The key features of Blockchain

Blockchain Technology is created to improve the limitations of traditional finance. Therefore, it is essential to understand the key features of blockchain that make it unique.

They are:

- Decentralization: One of the most important aspects of Blockchain Technology is that it is decentralized. This means that there is no central authority controlling or regulating the network. Instead, it is managed by a network of computers, known as nodes, spread across the globe. This decentralization makes it very resistant to fraud and corruption.

- Transparency: Another key feature of Blockchain Technology is its transparency. All transactions on the network are transparent and viewable by anyone with access to the network. This transparency helps to ensure that all parties involved in a transaction are honest and that there is no room for fraud or corruption.

- Immutability: Another important feature of Blockchain Technology is its immutability. This means that once a transaction is recorded on the network, it cannot be changed or deleted. This ensures that all transactions are final and cannot be tampered with.

- Security: Blockchain Technology is also very secure. All transactions on the network are encrypted and can only be accessed by those with the correct private key. This makes it very difficult for hackers to access or alter any data on the network.

- Efficiency: Blockchain Technology is also much more efficient than traditional financial systems. Transactions are processed almost instantly and there is no need for third-party intermediaries, such as banks, to be involved. This makes transactions much cheaper and faster.

- Scalability: One of the challenges facing Blockchain Technology is its scalability. The network can currently only handle a limited number of transactions per second. However, this is an area that is being actively worked on by developers and it is hoped that the network will be able to scale up in the future to meet the demands of its users.

- Distribution: Blockchain is unique in the sense that it is a distributed database. This means that it is not stored in one central location, but is instead spread across a network of computers. This makes it much more resistant to hacking and data loss.

- Smart contracts: A smart contract is a type of contract that is stored on the blockchain. This type of contract can be used to automate many different types of transactions. For example, a smart contract could be used to automatically send money from one person to another when certain conditions are met.

How does Blockchain work?

The structure of a blockchain is a chain of blocks, each of which contains a cryptographic hash of the previous block, a timestamp, and transaction data.

By design, a blockchain is resistant to modification of the data. Once recorded, the data in any given block cannot be altered retroactively without the alteration of all subsequent blocks, which requires the consensus of the network majority.

Blockchain structures can be used to store many types of data besides financial transactions. For example, a blockchain could be used to store data about identity, voting, or provenance. However, to fully understand the structure of blockchain, you need to understand what is a block.

A block is a record of some or all of the most recent transactions that have not yet been recorded in any prior blocks. Once a block is completed, it is added to the blockchain as a permanent database. Each time a new block is added to the blockchain, it becomes harder to change or delete the data inside of it.

Blocks have certain storage capacities and, when filled, are closed and linked to the previously filled block, forming a chain of data known as the blockchain. All new information that follows that freshly added block is compiled into a newly formed block that will then also be added to the chain once filled.

Types of Blockchain

There are four main types of blockchain networks: public blockchains, private blockchains, consortium blockchains and hybrid blockchains. Each one of these platforms has its benefits, drawbacks and ideal uses.

Public Blockchain

A public blockchain is a decentralized, distributed ledger that allows anyone to transact on the network without the need for permission from a central authority. This means that anyone can view, participate in, and contribute to the blockchain.

Public blockchains are open-source, meaning anyone can download the code and run a node on their computer to verify transactions. Bitcoin and Ethereum are examples of public blockchains.

Private Blockchain

A private blockchain is a digital ledger of transactions that is not open to the public.

Private blockchains are usually permissioned, meaning that only certain individuals or organizations can access them. They may be used within a single company or shared among a group of companies with similar interests.

Private blockchains offer some benefits over public blockchains, such as improved security and privacy. However, they also come with some trade-offs, such as reduced openness and transparency.

Permissioned Blockchain

A permissioned blockchain is a type of distributed ledger technology that restricts access to the network to authorized users. Permissioned blockchains are typically used by enterprises and organizations that need to control who can access their data and transactions.

One of the benefits of using a permissioned blockchain is that it can help ensure the security of the network by allowing only authorized users to access it. This can help to prevent data breaches and other security threats. Additionally, permissioned blockchains can offer improved performance and scalability compared to public blockchains because they do not need to process transactions from anonymous users.

Consortium Blockchain

A consortium blockchain is a type of distributed ledger that is jointly managed by a group of organizations, rather than by a single entity. This allows each organization to have control over its own transactions and data, while still maintaining a shared record of all activity. Consortium blockchains are often used in industries where multiple entities need to collaborate, such as in banking or supply chain management.

One advantage of consortium blockchains is that they can be more scalable than public blockchains, since there are fewer nodes that need to process each transaction. They can also be more flexible in terms of governance, since the rules for running the network can be decided by the group of stakeholders. However, consortium blockchains may be less secure than public blockchains, since the group of organizations that manage the network may be more susceptible to collusion.

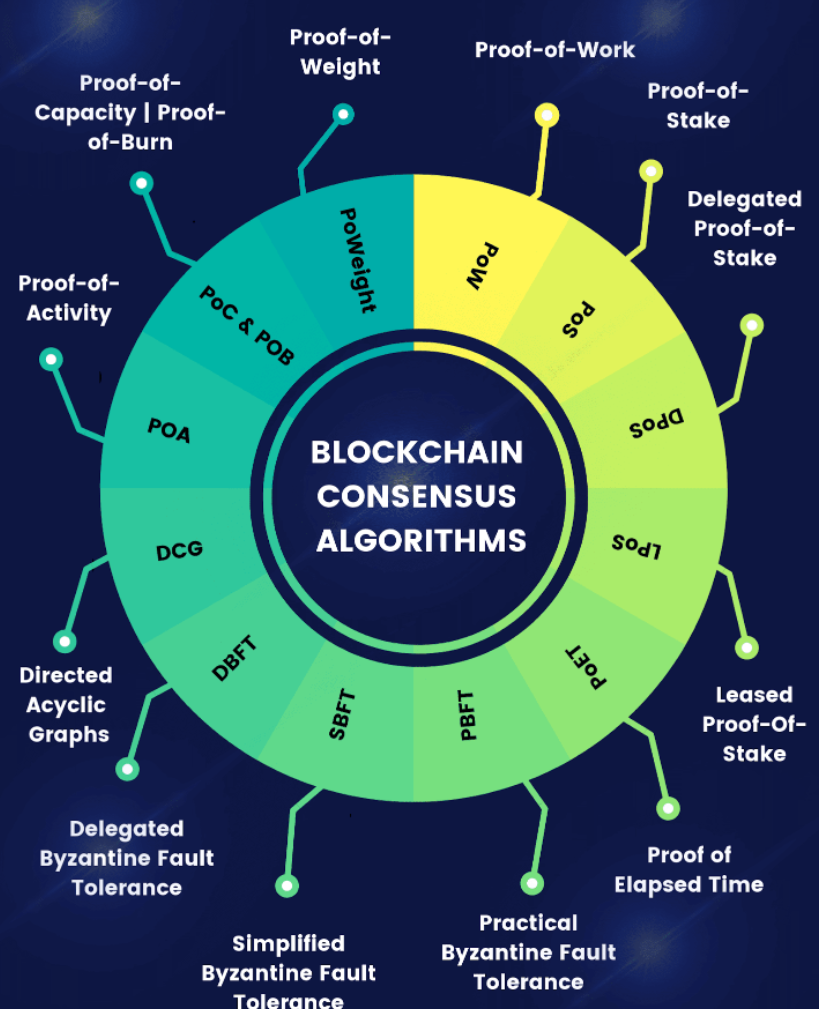

What is Blockchain Consensus?

Blockchain Consensus is a fundamental concept in the world of blockchain. It refers to the process by which all participating nodes in a network agree on the state of the ledger. This agreement must be reached before any transaction can be considered valid and added to the blockchain.

Proof of Work (PoW)

Proof of Work (PoW) is a type of algorithm used to verify transactions and prevent denial of service attacks. PoW algorithms require miners to solve complex mathematical problems in order to add new blocks of data to a blockchain. The miner who solves the problem first is rewarded with cryptocurrency. This process is known as "mining."

Proof of Work is used by many cryptocurrencies, including Bitcoin, Ethereum, and Litecoin. It is also used by some non-crypto currency systems, such as IOTA.

There are several advantages to using proof of work. First, it deters malicious actors from trying to modify or delete data in the blockchain, since they would need to redo all the work that has been done since the last block was added. Second, it allows for a decentralized system, since anyone can become a miner and earn rewards by contributing their computing power.

However, Proof of Work also has some disadvantages. First, it is energy-intensive, as miners need to use large amounts of electricity to power their computers. This can lead to environmental concerns. Second, it is slow, as it can take a long time for miners to find the solution to the mathematical problem. This can make some cryptocurrencies impractical for use in everyday transactions.

Proof of Stake (PoS)

Proof of Stake (PoS) is a type of consensus algorithm that allows a blockchain network to achieve distributed consensus. PoS is different from the more commonly used Proof of Work (PoW) consensus algorithm in that it does not require expensive mining hardware or large amounts of energy to secure the network.

Instead, PoS requires users to stake their coins in order to participate in the consensus process. The more coins a user stakes, the greater their chance of being chosen to validate a block and earn rewards. This makes PoS a more environmentally friendly and cost effective way to secure a blockchain network. Additionally, PoS consensus typically results in faster transaction times and higher scalability than PoW.

Delegated Proof of Stake (DPoS)

Delegated Proof of Stake (DPoS) is a consensus mechanism that was first used in the BitShares network. It is now also used by a number of other cryptocurrencies, including EOS and Steem.

In a DPoS system, there are a fixed number of "witnesses" who are responsible for validating transactions and maintaining the blockchain. These witnesses are voted in by the community, and they can be voted out if they are not doing their job properly.

DPoS was designed to address some of the issues with Proof of Work (PoW) systems, such as high energy consumption and centralization. With DPoS, only a small number of witnesses need to run full nodes, which makes the system much more efficient.

DPoS systems also tend to be more decentralized than PoW systems, as the witnesses are elected by the community. This means that there is no one person or organization who has control over the network.

Byzantine Fault Tolerance (BFT)

Byzantine Fault Tolerance (BFT) is a consensus algorithm that can be used to achieve consensus in a distributed system despite the presence of Byzantine faults. A Byzantine fault is a type of error that can occur in a distributed system, where some nodes may exhibit incorrect or malicious behavior. BFT algorithms allow for correct nodes to reach agreement on the state of the system even in the presence of Byzantine faults.

There are several different variants of BFT algorithms, each with its own strengths and weaknesses. Some popular BFT algorithms include PBFT, SBFT, and RAFT. In general, BFT algorithms are more complex than other types of consensus algorithms (such as Proof-of-Work or Proof-of-Stake), and thus require more resources to run. However, they offer a higher degree of safety and security, which makes them well-suited for applications where safety is critical, such as in blockchain systems.

Proof of Authority (PoA)

Proof of Authority (PoA) is an alternative consensus algorithm that is much faster and cheaper. With PoA, a set of validators (referred to as "authorities") are chosen to validate transactions and add new blocks to the blockchain. These authorities are typically selected by the people who run the blockchain network.

One advantage of PoA is that it is much more energy-efficient than PoW. This is because there is no need for miners to use their computational power to solve math problems. MakerDAO, ZIN are common projects that used PoA consensus.

Proof of Weight (PoWeight)

Proof of Weight (PoWeight) consensus is a new consensus algorithm that promises to be more secure, efficient, and scalable than existing algorithms. PoWeight is based on the concept of "weighted proof of work" (WPOW), which combines the best aspects of both proof-of-work (POW) and proof-of-stake (POS) systems.

Unlike POW or POS, PoWeight does not require users to have expensive hardware or large amounts of capital to participate in the network. Instead, users can choose to either provide their computing power to the network or purchase tokens that represent a unit of weight.

The more weight a user has, the more influence they have over the consensus process. This makes PoWeight a more democratic and inclusive consensus algorithm that is accessible to everyone.

PoWeight is also more energy efficient than POW or POS, as it does not require users to waste resources on mining or staking. Therefore, PoWeight is designed to be highly scalable, as its consensus process can be parallelized across multiple computing nodes. This makes it well suited for large-scale applications such as decentralized exchanges (DEXs) and social networks.

Proof of History (PoH)

Proof of History is a method of establishing consensus on the order of events in a distributed system. This is accomplished by having each participant in the system commit to a hash of all previous events in the system; this hash is then used to determine the ordering of future events.

There are several benefits to using PoH over other protocols. One is that it can be used to achieve consensus on very large data sets, such as those involved in big data analytics. Additionally, PoH is more energy efficient than PoW, and it doesn't suffer from the same security risks as PoS.

Proof of Reputation (PoR)

A reputation system is a way of measuring the trustworthiness of an individual or entity. In the context of Blockchain Technology, a Proof of Reputation (PoR) consensus algorithm uses a reputation system to determine which nodes are allowed to validate transactions and add blocks to the blockchain.

Nodes with a good reputation are more likely to be trusted by the network and given the opportunity to validate transactions and add blocks. Nodes that don't have a good reputation may be excluded from participating in consensus, which can lead to them being cut off from the network and missing out on rewards.

Proof of Reputation consensus algorithms can be used to create more decentralized and secure blockchain networks, as they allow anyone with a good reputation to participate in consensus. This can help to prevent centralization and improve security.

PoR consensus algorithms have been used by some of the largest and most popular blockchain networks, including GoChain Coin (GO)...

Real-World Applications of Blockchain Technology

Blockchain is a disruptive technology that has the potential to revolutionize many industries. But it's not always easy figuring out how this new tech will affect our lives on an everyday basis - or even if there are any real-life uses for something so revolutionary.

Well, as it turns out, there are actually quite a few blockchain applications that are already being used in the real world. Here are just a few example:

Medical records: One area where blockchain could have a big impact is in healthcare, specifically in the way medical records are managed. At the moment, patient data is often spread across different systems and databases, which can make it difficult to get a complete picture of someone’s health history. Blockchain could be used to create a secure, decentralised system for storing and sharing medical records, which would make it much easier for doctors and other healthcare professionals to access the information they need.

Supply chain management: Another potential use case for blockchain is in supply chain management. The supply chain is the system that ensures goods and materials are moved from one place to another, and it’s often a complex process with many different stakeholders involved. By using blockchain to track items as they move through the supply chain, businesses can get a more transparent and efficient way of managing their supply chains.

Digital identity: Another area where blockchain could have a big impact is in digital identity. At the moment, our online identities are managed by centralised organisations like banks, social media platforms and governments. But what if there was a way to manage our digital identities in a decentralised way? That’s where blockchain comes in. By using blockchain to store identity data, we could have more control over our personal data and who has access to it.

Banking system: The banking system is another area where blockchain could have a big impact. Blockchain could be used to create a decentralised, peer-to-peer banking system that would be more efficient and secure than the current system. This would give people more control over their finances and make it easier to transfer money between different countries.

These are just a few of the potential blockchain applications that are already being used or developed in the real world. As Blockchain Technology continues to evolve, we’re likely to see even more practical uses for it in our everyday lives.

The Evolution of Blockchain

The Blockchain Technology has evolved quite quickly over the years. These brief descriptions below will explain the development of Blockchain Technology.

Blockchain 1.0 - Currency

In simple terms, Blockchain 1.0 refers to the first generation of Blockchain Technology which was created for the sole purpose of powering digital currencies. Bitcoin, the first and most famous cryptocurrency, was built on a Blockchain 1.0 platform.

Blockchain 1.0 platforms are typically quite basic and rudimentary in comparison to newer generations of Blockchain Technology. However, they remain incredibly popular due to the fact that they are incredibly secure and offer a high degree of immutability.

Blockchain 2.0 - Smart Contracts

The new key concept in the blockchain-world are Smart Contracts. To put it simply, a smart contract is like a normal contract, but with one important difference: it is automatically enforced by code. This means that if one party doesn't hold up their end of the bargain, the other party can enforce the contract automatically..

Blockchain 2.0 –Smart Contracts could potentially transform many industries and make our lives easier by eliminating the need for third-party intermediaries in a wide variety of transactions. The most prominent project that used smart contracts is the Ethereum blockchain.

Blockchain 3.0 - Decentralized Applications

A Decentralized Application (DApp) is a computer application that runs on a distributed computing platform. A DApps can be coded in any programming language that can communicate with a blockchain. DApps have its backend code running on a decentralized peer-to-peer network. Contrast this with an app where the backend code is running on centralized servers.

The term "DApp" is often used interchangeably with "smart contract". A smart contract is a piece of code that runs on a blockchain and defines certain rules around an agreement or transaction. A DApp is essentially a smart contract with a user interface.

User experience can vary widely for DApps, from simple command-line applications to complex graphical interfaces. The important thing is that the application is decentralized, meaning the backend code is running on a decentralized network rather than centralized servers.

Blockchain 4.0 - Practical Usage

From cryptocurrency to smart contracts, this distributed ledger technology has the potential to change the way we interact with data and conduct transactions. This latest iteration of Blockchain Technology is often referred to as the "fourth industrial revolution" or "Industry 4.0."

It takes the idea of a distributed ledger and builds on it, integrating new technologies like artificial intelligence (AI), internet of things (IoT), and big data. This allows for more complex applications and higher levels of security. The Blockchain Technology 4.0 will be applied in all areas of the digital economy

Is Blockchain safe?

With all the mentioned features of Blockchain Technology, we can say blockchain is pretty safe. The technology is designed to be secure, and its decentralized nature makes it difficult for hackers to target.

Additionally, each transaction is verified by multiple nodes on the network, making it nearly impossible to tamper with data. There is no single point of failure on the blockchain, which makes it a very secure platform.

The blockchain also uses cryptography to secure its data which is a process of converting readable data into an unreadable format. This makes it difficult for hackers to access the data. Additionally, each block in a blockchain is linked to the previous block.

This makes it nearly impossible to alter the data without changing all of the subsequent blocks. Finally, blockchain is decentralized, meaning that it is not controlled by any one entity. This makes it resistant to tampering by central authorities.

Is Blockchain the future?

With the technological advances of recent years, it's no surprise that blockchain has been gaining popularity as a potential game-changer across a number of industries. But what is blockchain, and what could it mean for the future?

In its simplest form, a blockchain is a decentralized database that stores information in a secure way. This means that there is no central authority controlling or managing the data - instead, it is spread across a network of computers, known as "nodes". Because each node has a copy of the entire database, this makes it virtually impossible to hack or tamper with.

This security is one of the main reasons why blockchain is seen as having so much potential. For example, in the financial sector, blockchain could be used to create a secure and transparent way of handling transactions. This would not only reduce the chances of fraud or corruption but could also speed up transaction times and make them more efficient.

Similarly, in the healthcare industry, blockchain could be used to store patient records in a secure and tamper-proof way. This would not only protect patient privacy but could also help to improve the efficiency of healthcare delivery.

There are many other potential applications for Blockchain Technology, and it is still in its early stages of development. However, it is clear that blockchain has the potential to revolutionize a number of industries - making it one to watch in the years to come.

Investment opportunities with Blockchain

The rise of Blockchain Technology has been nothing short of meteoric. In just a few short years, this new form of distributed ledger technology has gone from being an unknown concept to one of the most talked-about topics in the tech world.

And it's not hard to see why. Blockchain offers a unique set of benefits that make it perfectly suited for a wide range of applications. From its immutability and security to its decentralization and transparency, blockchain is poised to revolutionize the way we do business.

As such, it's no surprise that investors are clamoring to get in on the action. But if you're thinking about investing in blockchain, it's important to understand how this new technology works and what it could mean for your portfolio.

There are many ways to invest in Blockchain Technology. Here are a few options:

- Invest in a blockchain company.

- Invest in a cryptocurrency.

- Participate in DeFi to earn profits such as yield farming, providing liquidity for a platform...

- Buy and sell NFTs on marketplaces to make profits.

- Playing gamified projects to earn rewards.

Conclusion

Blockchain is becoming more popular and is gradually having more practical applications. Through this article, I hope you have gained useful information about blockchain as well as other valuable insights.

Please register and join Coin98 Insights groups and channels below to discuss with admins and other community members.

Also available in

Vie