Crypto Market Report H1 2022

The crypto market had a lot of difficulties in the first half of 2022, one of the most challenging times in the last 2 years. Terra, one of the largest ecosystems in the crypto market collapsed. Besides that, many native organizations in crypto fell into a state of "forced selling", trading activities and volume plunged, …

Key Insights:

- The US government has implemented a quantitative tightening (QT) monetary policy to minimize excess cash from the economy.

- Crypto markets are highly correlated with the US economy, fluctuating similarly to high-risk assets. As a result, when the US government carries out QT, the crypto market tends to go down more sharply than other financial markets.

- The bad macroeconomics; the crypto market's poor attraction of new cash flow; the collapse of Terra, Three Arrows Capital, Celsius, and many other large and small institutions made the crypto market fall into a deep bearish state.

- New trends in the future will be set up based on old issues which have not been resolved in the past bull run section. This is a typical problem of blockchain scaling.

Macro overview in H1 2022

The FED implemented a quantitative easing (QE) monetary policy, "adding" about $4,600 billion into the market with the aim of pushing economic growth after the lockdown time of the Covid-19 pandemic.

Lowered interest rates made capital expenditures cheaper, playing a part in enriching liquidity for financial assets. This ideal environment is for risky assets like technology stocks or the crypto market. It makes the average ROI in the market mostly positive:

- The ROI of Bitcoin reached 1,700%, and the total market cap increased by 2,000%.

- Gold gained 40%.

- Stock increased 110%.

However, Inflation has occurred due to QE monetary policy and political conflicts, so, central banks were forced to tighten quantity (QT) by withdrawing excess currency from the economy.

The main characteristics of the macroeconomic environment and the financial market in general for the years 2020 to 2022 are summarized in this section. We will highlight some noteworthy events that will impact the macro environment in the first half of 2022 in the following parts.

Russia and Ukraine are engaged in political turmoil

The political conflict between Russia and Ukraine has had a negative effect on the overall economy. The prices of oil, food and other commodities rose as the West imposed sanctions on Russia.

As a result, supply chains are disrupted, costs increase, and inflation occurs. Since then, the FED and central banks planned to raise interest rates and apply tight monetary policy to diminish the above situations.

Specifically, the price of Brent oil has surged by ~46.6% in the first 6 months of the year. The price has spiked 30% since Russian President -Vladimir Putin announced the special military operation in Ukraine on February 24th.

Although the oil price has dropped (about 14% from its peak within 3 months), it is still unstable as it is affected by other factors such as political situation or OPEC not being able to supply more oil production.

Not only affecting oil prices, the war also caused food prices to rise (especially in the European region) as Russia and Ukraine are at the top of exporting wheat to the world. Crude oil is also an important production input for the agricultural industry.

It is very clear that people must reduce spending because of political purposes in the world. Data from the US Bureau of Economic Analysis has shown that the growth rate of people's spending in this country is at the lowest level since 2021.

People are forced to spend more money to cover their basic needs due to rising prices and personal struggles. The result will be a dearth of cash flow from retail investors in the financial markets as savings and investment dwindle.

The economy is in trouble

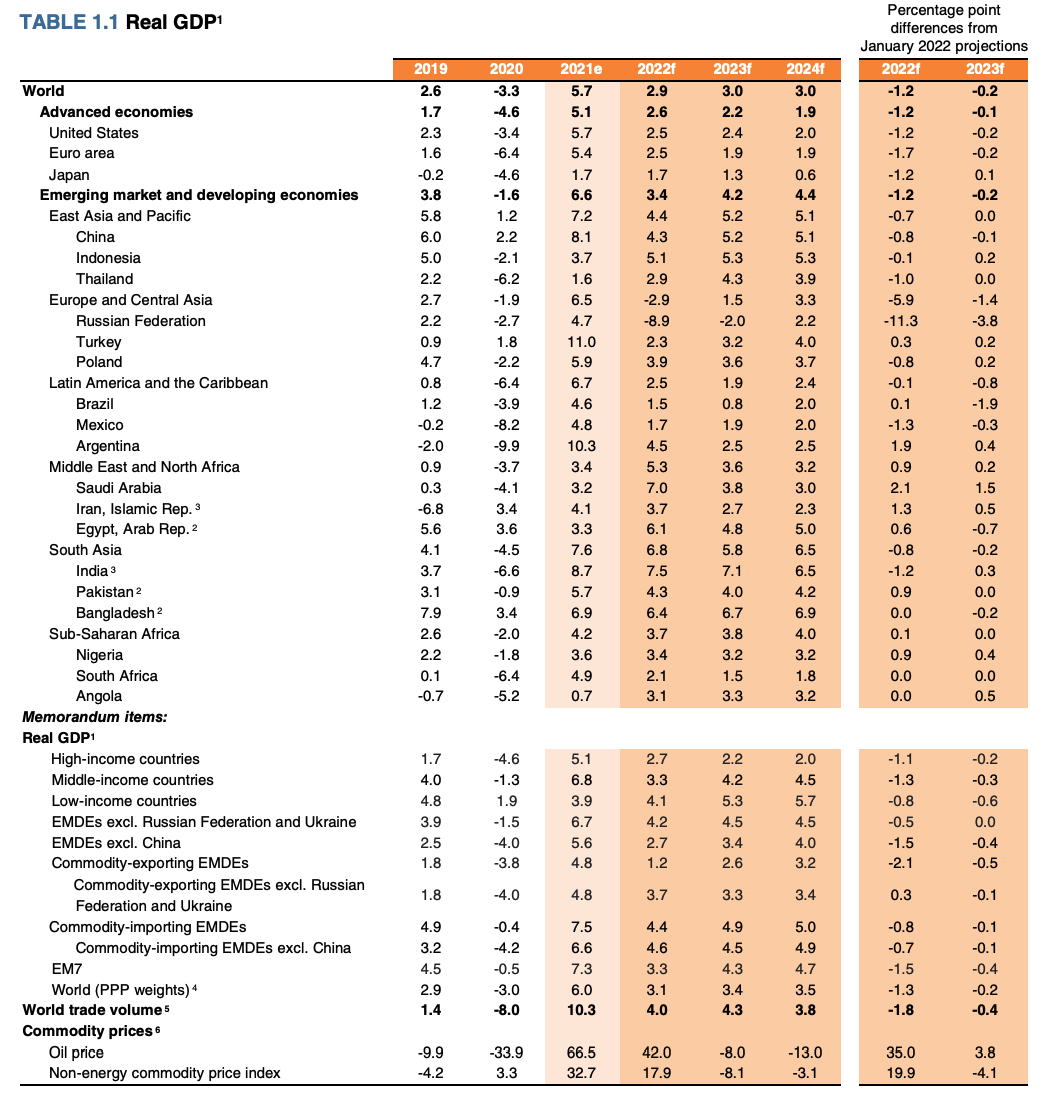

War and political conflicts have had a negative impact on the global economy. According to a forecast from the World Bank, global economic growth will be flat in the 2022 - 2024 period with GDP growth in the range of 3%.

Global GDP growth forecast in 2022 has been revised down by the World Bank by 1.2% (compared to the forecast from January when there was no conflict between Russia and Ukraine).

Details of the World Bank report can be found here.

The current economic situation is compared by many experts to the 1970s when the stagflation occurred.

On one hand, the oil supply shock caused rising prices. The 1970s led to a decline in economic growth and this situation is happening again in 2022.

However, governments have historical data at their disposal, enabling them to align their fiscal and monetary strategies with the current economic statement.

In addition, central banks raised interest rates to curb inflation, which negatively affects economic growth. As a result, capital will return to strong currencies in developed economies, causing developing countries (with faster GDP growth) to lack the resources in order to reach their full potential.

Another forecast from the World Bank shows that global inflation data will start to go down from the third quarter of 2022 and gradually stabilize at 2% - 3% from 2023.

However, the economic situation is still unlikely to return to steady growth from 2023.

According to the distribution chart of global GDP growth projections, the baseline GDP growth scenario in 2023 is 3% with a 50% rate that will range between 1.6-4%.

Therefore, even under the baseline scenario, we are still unlikely to see growth again in 2023 as well as the potential risk of further decline, but if governments can end the conflict with appropriate policies, a brighter picture for the global economy can still take place.

The FED's QT

After the December 2021 FOMC, the FED made a decision to start QT from the beginning of 2022 with the interest rate until the end of the year planned at ~0.9%.

Unfortunately, this decision could not be made due to the war between Russia and Ukraine. The FED must raise interest rates to make the current situation better.

The latest US inflation data (updated on June 10) was 8.6%, the highest since 1981.

High inflation since the war between Russia and Ukraine has forced the FED to raise interest rates with the aim of cooling down commodity prices.

The Dot Plot chart in the Fed's latest meeting in June has made this point clearer.

Specifically, policymakers have supposed the FED's interest rate is in the range of 3.1% - 3.9% in 2022 based on indicators and forecasts for inflation, GDP growth and unemployment. It has increased 3-4 times compared to the number given at the meeting at the end of 2021, negatively affecting most financial assets (stocks, bonds, crypto...)

According to Bloomberg, the FED is expected to shrink its balance sheet by about $5,000 billion in the period from 2022 to 2026, of which:

- $600 billion in 2022.

- $1,000 billion in 2023.

- $3,000 billion in 2024-2026.

However, according to the Dot Plot chart above, the FED is likely to loosen monetary policy again from 2024 onwards to stimulate the economy after the current difficult period. Therefore, it is possible that the shrinking $5 trillion target figure will not be realized.

On the other hand, easing money accompanied by expanding the FED's balance sheet will be a better environment for the growth of assets such as stocks, real estate, crypto …

Negative line of asset classes

Inflation has a negative impact on assets including stocks, gold, bonds, and cryptocurrency due to the Fed's and other central banks' tightening monetary policies.

The S&P 500 index (representing the 500 largest companies by market capitalization on the US stock exchange) has recorded a ~21% drop since ATH and a ~19.88% drop from the beginning of the year until now (in the stock market).

As interest rates rise and cash flow is reduced, businesses' costs rise and their profit margins are impacted. This is the primary cause of the stock's precipitous decline.

Bonds are always rated as a safe and low-risk asset, but also due to macro factors, they become unattractive.

The US government’s bond yield continued to maintain an uptrend, showing that bond sales are accelerating under the influence of interest rate hikes and the FED's bond sales to shrink its balance sheet.

In contrast to stocks, the real estate market remains high (for house prices) as a result of the previous low interest rate environment. The US home price index, although growth has slowed down, is still at a high level. The growth rate in 2021 is even greater than the pre-bubble period in 2004.

In addition to the US, the OECD has issued severe warnings about rising property prices in numerous other nations, including New Zealand, Canada, Australia, etc.

The housing market is always at risk as debt and liquidity problems pose a risk to the economy. In fact, there are still countries where the real estate situation is very hot.

Rising house prices also have a direct impact on people's income and savings as they have to bear higher costs of accommodation.

Gold price movements in 2022 were highlighted in the event of political conflict between Russia and Ukraine with an increase of 13.6% within 1 month from the beginning of February to March.

However, the gold price has cooled down due to the effects of tight monetary policy (from the beginning of the year until now), gold has almost no change in price, only increasing by 0.2%.

Thus, when looking at the macro factors, it can be seen that when the economy goes down, people's income and savings decline and financial assets can hardly grow. Although there are still some asset classes that have increased in price such as real estate or commodities and food, they are not only negative factors but also pose certain risks to the economy.

In that context, investors have lost interest in high-risk investments like cryptocurrency. Additionally, the biggest crypto institutions in the market are also impacted by the weakening market environment and rising costs, which has led to negative consequences like staff layoffs, a shortage of liquidity, increased use of borrowing, etc., and the near-bankruptcy of many companies.

Summary of macroeconomic & political situation in the first half of 2022:

- The war between Russia and Ukraine took place as an event that greatly affected the economy, making people's lives difficult, the cost of basic goods increased, causing savings and investments to decline.

- The FED and central banks globally implemented quantitative tightening leading to less abundant liquidity in the market.

- In that context, financial assets such as stocks, bonds, gold, etc. showed weak performance. Although the real estate market is still in an uptrend, this growth poses risks to the economy.

In short, it seems that investors in the market have been "priced in" based on the macro variables analyzed above, but there are still many risks ahead, requiring defensive moves in portfolios. Investments in this period must continue to be highly appreciated.

Crypto market in H1 2022

Key highlights impacting the market

Year-to-date, Bitcoin has seen a 57.8% drop. This is followed by a decline in market capitalization of about 70% since ATH (equivalent to more than 2,000 billion USD).

Besides, we can also mention the outstanding events that contributed to the above decline such as:

- The event of UST (Terra ecosystem's stablecoin) losing its peg caused Luna Foundation Guard to sell BTC in its Treasury to subsidize UST.

- Celsius events with consequences leading to asset liquidation on Lending protocols causing price drop.

- Three Arrows Capital being in danger of bankruptcy led to many uncountable consequences behind it.

The collapse of Terra (LUNA) and its ecosystem took a heavy toll on the parties involved. So far we do not have an overview of the damage to Terra (LUNA), the ecosystem, and the parties that have suffered around UST.

This event creates selling pressure in the crypto market (OTC, secondary market...), and affected parties tend to reduce the proportion of positions for the purpose of portfolio rebalancing.

Through lending & debt protocols, additional “money” is generated, and the loss of investment in Terra (LUNA) & the ecosystem around UST highlights the payment risk to the parties involved.

The LUNA & UST events triggered a domino fall for parties like Celsius, Three Arrows Capital... These are absolutely not small organizations in the market, and when they face difficulties, many stakeholders will be involved. Therefore, it is too early to conclude that the influence has ended.

The macroeconomic environment is generally unfavorable for the cryptocurrency market. Liquidity concerns and a downturn in demand, along with the lack of many new groundbreaking items, are what caused the market to fall.

- Liquidity risk: Manifested in Staked assets (such as stETH), deals from the primary market (leading to Three Arrows Capital's illiquidity), LUNA not being liquid enough to hold Peg for UST…

- Declining market demand: This aggravates the situation that liquidation can occur without liquidity causing a sharp drop in price (very evident in the event of Solend taking over users’ wallet management).

Poor risk management is the main reason leading to the above consequences. This also shows that large organizations that manage billions of dollars when entering this market have not yet fully assessed the potential risks.

⇒ The cryptocurrency market has grown (with a market capitalization of $3 trillion USD), but is still in its infancy.

Besides, the fact that whales holding a large amount of Bitcoin in the market today such as Microstrategy, Tesla or El Salvador are recording losses making the investor sentiment even more negative. Especially for those under debt pressure like Microstrategy, when the amount of BTC they hold is liquidated, it will be more likely to cause a sharp drop in price because the liquidity in the crypto market is quite thin right now.

In general, there have been comments that without chain effects such as Terra (LUNA), Celsius, or Three Arrows Capital, Bitcoin is likely to remain in the $35,000-$40,000 price range for the time being.

The trade-off between growth and security

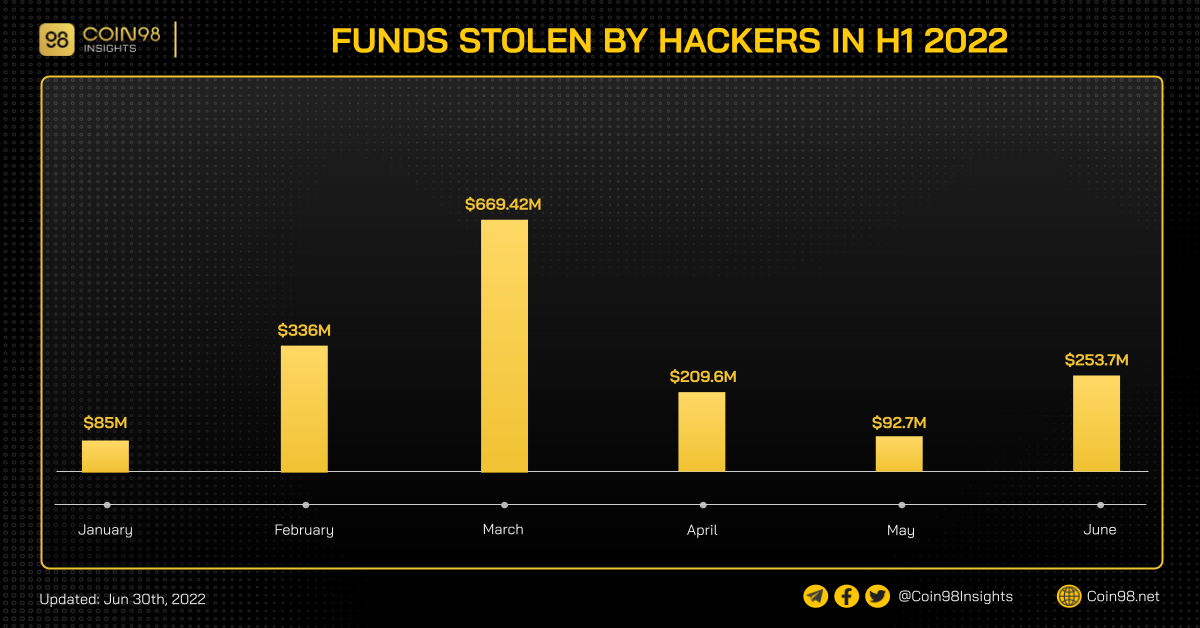

The level of hacked projects in the first half of 2022 raises numerous concerns about the trade-off between rapid growth and security.

According to The Block, the first half of 2022 is the period when hack/exploit events with the highest asset value were recorded.

In the first half of 2022, the attackers stole approximately $1.6 billion.

Up to 4 out of every 6 months, assets worth more than $200 million USD have been lost. In detail, there was a spike in damage in February and March due to two major hacks in the Bridge array (Wormhole and Ronin Bridge).

Statistics of attacks by ecosystem show that Non-EVM and EVM Compatible blockchains suffered a greater amount of damage. Specifically, Ethereum-related cases account for only 17.7% of the value, while Non-EVM and EVM Compatible blockchains have 29.9% and 52.4%, respectively.

Learn more: What is EVM Compatible blockchain?

Although investing in layer 1 blockchains (Non-EVM and EVM Compatible) yielded very good returns in 2021, once the growth season has passed, these ecosystems revealed many security flaws.

This directly affects users' trust in the protocols in the ecosystem, thinning the liquidity of the crypto market, and making the Bear Market situation worse.

To summarize, the crypto market in the first half of 2022 has the following key features:

- The market, in general, turned negative and there was not much "room" for growth due to the negative impact from the macro side.

- Terra, Celsius, Three Arrows Capital, and other events put pressure on the market. These events also highlighted the flaws in crypto institutions' risk management.

- The series of hacks/exploits are the result of a trade-off between rapid growth and a lack of security.

On the other hand, the bear market is a “stress test” to find new investment opportunities with long-term growth potential.

Key categories analysis

In the next part, we will dive deep into key categories of crypto market in the first half of 2022, including the following:

- Focusing on Rollups instead of Alt-L1.

- Not “DeFi era” anymore.

- NFT continues to be the “black hole”.

- Limitations and solutions of DAO.

Focusing on Rollups instead of Alt-L1

DeFi on Ethereum exploded in Q1/2020 causing the average gas price on Ethereum to fluctuate strongly in the range of 100 - 300 Gwei. With such gas prices, the average transaction fees for basic DeFi operations such as approval, swap and adding liquidity often exceed $100.

Alt-L1s are temporary alternatives where other scaling solutions are not ready to go. Some notable Alt-L1s in 2021 include:

- EVM: BSC, Polygon PoS Chain, Fantom, Harmony, Avalanche C-Chain.

- Non-EVM: Terra, Solana, Near.

In general, Alt-L1 ecosystems often compete with each other around issues such as low transaction fees, high throughput, low latency, and ecosystem incentives (funding & subsidies). However, over the period of operation, Alt-L1 revealed certain limitations. Basically, they trade off one or more important features such as security and decentralization in exchange for low fees and instant scalability.

If the story in 2021 around “Alt-L1 solved the blockchain scaling problem, Ethereum sharding & rollup is too little, too late”.

Going through 2022, the story has changed drastically, “Alt-L1s can't scale, most have structural issues, sharding & rollup is the most viable to scale blockchain in time next”.

Although sharding and rollup have many advantages, they do have some limitations in terms of time, ownership, and governance. A typical example is the dYdX event announcing the project's move to a Cosmos-based chain.

It is difficult to say which solution or development direction is suitable for the market in the next 6-18 months. However, we can be sure that the stories surrounding the topic of “increasing the performance of blockchain” remain one of the main stories for the next bull run.

Not “DeFi era” anymore

Before 2021, DeFi mainly developed on Ethereum and Ethereum’s DeFi dominance accounts for more than 95% of TVL.

During this time, the Ethereum DeFi market has grown at an exponential rate. Within this period, a number of DeFi primitives protocols have launched and grown the network, laying the groundwork for DeFi's development on Ethereum. Typical projects include:

- On-chain liquidity: Uniswap.

- On-chain lending: Compound, Aave.

- Debt market: Maker DAO.

In 2021, the DeFi market on Ethereum is no longer the center of the story. DeFi development is mostly horizontal and the focus is on Alt-L1s (EVM Chain & non-EVM Chain). However, other blockchains are mainly forking the development direction of the DeFi market on Ethereum, with no new breakthroughs being created in the market:

DeFi on BSC:

- Uniswap (Ethereum) ⇒ Pancakeswap (BSC).

- Compound, Aave (Ethereum) ⇒ Venus (BSC).

DeFi on Polygon PoS Chain:

- Uniswap (Ethereum) ⇒ Quickswap (Polygon).

- Compound, Aave (Ethereum) ⇒ Aave (Polygon).

This development led the total TVL of the crypto market to surpass $300 billion in 2021. However, the unhealthy development of the DeFi market, plus the negative effects from the macroeconomics made DeFi fell to stagnation.

The total TVL of the whole market was flat throughout Q1/2022. The collapse of the Terra ecosystem is the trigger for the “domino fall” event of the crypto market. Currently, the DeFi market is in a contraction phase, activities are focused on only a few leading categories in the market:

Stablecoin

In Q2/2022, stablecoin market capitalization had a big decline, decreased by nearly $ 50 billion (nearly 25%) when compared to the ATH achieved in 2022. In the stablecoin segment, we can divide them into 2 groups:

- Fiat-backed stablecoin: BUSD, USDC, USDT,...

- Crypto-backed stablecoin: MIM, FRAX, UST, FEI,...

The collapse of the stablecoin market comes from both groups. Fiat-backed stablecoins’ capitalization plummeted but still accounts for more than 90% of the market share. Fiat-backed stablecoins’ decrease showed the negative impact of monetary policies to the crypto market.

A large drop was recorded in the crypto-backed stablecoin group. This is evident in the drop in supply of some of the top crypto-backed stablecoins from their ATH levels in Q2/2022;

- UST de-pegged, market capitalization lost more than 99%.

- MIM’s supply dropped by 92.94%

- DAI’s supply declined by 25.41%

- FRAX’s supply plunged by 48.15%

One of the primary drivers for the development of crypto-backed stablecoins is the need for leverage on assets held via the Defi market's debt and lending protocols.

The collapse of the Terra ecosystem, Three Arrows Capital, and the negative effects of the macroeconomic impact caused liquidity in the crypto market to become more serious. Investors also begin to reduce the number of crypto assets that they hold to avoid the risk of liquidation

Hence, the fall in the supply of crypto-backed stablecoins is understandable given that one of the primary reasons that fueled their creation is no longer pressing.

Decentralized Exchanges (DEX)

DEX is an important piece of the puzzle and a place where liquidity can be created for the market. The development of all financial markets is based on ample liquidity. DEX is divided into two major categories: AMM & Order Book.

In which, the majority of DEXs on chains are implementing the AMM model. However, the DeFi market is in a contraction phase and activities are concentrated on a few leading chains in the market like Ethereum & BSC.

Uniswap is the leading AMM in the DeFi space. It allows users to swap their assets through liquidity pools (LPs) contributed by users. The prices of the assets in the pool are determined by a predefined algorithm of x*y = k.

Uniswap is one of the protocols that started the development trend of DeFi on Ethereum. Up to now, Uniswap has gone through 3 main stages of development;

- 2017 - Uniswap V1, allowed users to create pools with ETH (ERC20-ETH).

- 2020 - Uniswap V2, the highlight of this upgrade is allowing users to create a liquidity pool between any 2 tokens (ERC20-ERC20).

- 2021 - Uniswap V3, an upgrade that allows Uniswap to use capital more efficiently. Some outstanding additional features include: providing centralized liquidity, flexible fees, and smart order routing,...

Pancakeswap is the native AMM on BSC. It is currently the DEX with the highest trading volume on BSC. The core feature of Pancakeswap is forked from Uniswap v2. Besides, the project has also developed many additional features such as Syrup Pools, IFO, Lottery, Team Battle, etc. to encourage users to provide liquidity and trade on Pancakeswap.

Curve Finance is an AMM optimized for trading stablecoins or crypto assets of equal value (e.g. sBTC, renBTC, wBTC…). Curve Finance is one of the projects that offer many innovations in terms of economic design for the project's native token, typically the veToken model.

In addition to some of the AMMs highlighted above, there are a few creative ideas on the AMM design in the market, which can be a bright spot for the future development of AMM. Three typical projects include:

Crocswap (AMM runs on a single smart contract):

- Typically, each AMM liquidity pool is managed by a separate contract. Crocswap proposes the idea of building an AMM that runs on a single contract. In this contract, there will be many lightweight data structures representing individual liquidity pools.

- In addition, this design also brings advantages of gas fee when trading and balances liquidity. This design allows Crocswap to open up many potential applications for AMM.

Muffin (an AMM that offers multiple rates per pool):

- Some AMMs like Uniswap have a flat fee of 0.30% while others offer 1 or 2 fees per group. If users want more rates, they must create a new group. Muffins give LPs more granular control over their positions.

- Muffin has created a model of multiple fees per liquidity pool. In a liquidity pool, there can be up to 6 choices of fees.

- Depending on the state of the market, LPs can choose the price range and fees they want to provide liquidity.

YieldSpace (a custom AMM used to liquidate the fytoken/token pair to create fixed rate markets):

- YieldSpace is a custom curve with a variable t to accommodate liquidity for the fytoken/token pair to create fixed-rate markets.

- Of which, t is a time variable, larger t means longer maturity. As the expiration date approaches, t approaches 0. Here is the general formula of YieldSpace:

Lending & Borrowing

The lending and borrowing market, in addition to DEX, is the foundation for the development of DeFi. This market is created by two large project groups, Lending Protocol and Debt Protocol. These protocols enable borrowing and lending by allowing users to pool their assets in a common asset pool (Peer to Pool).

Learn more: What is Crypto Lending?

In the first half of 2022, borrowing and lending activities decreased sharply, reflected in the total TVL and total outstanding loans of the market when compared to the beginning of Q1/2022.

- Total TVL $18.55 billion, declined by 64.67%.

- Total outstanding loans $10.3 billion $, down by 63%.

In which, Maker, Aave, Compound are the top three markets in the field with outstanding loans respectively;

- Maker market $6.3 billion.

- Aave market $1.75 billion.

- Compound market $0.8 billion.

The current lending and borrowing market is mainly driven by projects with similar designs (Peer to Pool model). One of the limitations of these models is that they generate highly volatile free floating-rate loans.

The level of uncertainty and volatility in the DeFi market is not beneficial to long-term financial planning and leveraged investments, indirectly preventing DeFi's growth to a larger market size. With advancements in fixed-rate markets, this could be critical to the further evolution of the lending and borrowing market.

Liquid Staking

Operating a validator in PoS blockchains is often quite difficult. In addition to the technical requirements, the project often requires staking & bonding a relatively large amount of tokens of economic value. These tokens are locked within the network and cannot be used outside.

Liquid Staking is the solution to this problem, when a user stake their tokens into a Liquid Staking protocol, the user will receive a corresponding amount of staked tokens, representing the amount of tokens they have staked in the system. These staked tokens can be used for trading, lending, or providing liquidity for additional profit.

Liquid Staking mainly developed on Ethereum. Their development is driven by the complexity of running an Ethereum validator. It requires users to run specialized software, staking 32E, minimal computer hardware.

Beside the difficulty in launching, managing and ensuring the node works stably to avoid slashing is even more difficult. In general, not many people have enough of those requirements.

Liquid Staking protocols provide a solution to the above problem by dividings users into 2 main components:

- Depositors: Capital Contributor (ETH)

- Node operators: Technical contributors who could run and maintain nodes.

The technical elements are taken care of by node operators. While the capital element is maintained by depositors, both groups will work together to mine the block reward on Ethereum and split the profits with each other.

Currently, the top two players are Lido and Rocket Pool, respectively. Lido uses 29 professional node operators. However, this approach raises a new problem of centralization, as 29 Node operators control ⅓ of the voting power on Ethereum.

Rocket Pool promises a more decentralized Liquid Staking solution, by requiring each operating staking node, node operators must stake 16 ETH to bind the benefits of node providers to the system, avoiding the status of nodes. Providers act in a way that is not in the general interest of the network. The remaining 16 ETH was raised from depositors.

However, this makes Rocket Pool's solution harder to scale than Lido's because not all node operators have large amounts of ETH to operate, with the merge likely happening in September of this year, the story around the topic of liquid staking may be more important than ever.

NFT continues to be the “black hole”

NFT stands for Non-fungible Token, which is a unique token and cannot be replaced by others. 2021 was an explosive year for the NFT market and there have been many life-changing stories written since. So will this continue in 2022?

NFT market overview in H1 2022

Q1/2022 continues to witness a strong boom of the NFT market. In Q2 due to the general trend, the NFT market experienced a decrease in indicators such as price and trading volume. However, NFT has proven its potential and attracted many projects in this field.

A recent example can be mentioned that today's largest AMM exchange, Uniswap, has acquired Genie, a project that aggregates NFTs on many NFT marketplaces. Arbitrum announced weekly quests with NFT rewards. Zapper announced that NFT is the focus and many other projects are also using NFT in their products.

NFT has a large percentage of attention globally. The number of searches for the keyword “NFT” on Google surpassed important keywords such as “ETH” and “blockchain”. Between 2021 and Q1/2022 is a period of strong growth for NFT.

The explosion of NFT has sparked the growth of numerous adjacent fields. Some of the most prominent are:

- NFT Collectibles

- NFT Gaming

- NFT ecosystems and their internal categories

NFT Collectibles

The first major application of NFT was the creation of artworks. With special characteristics such as uniqueness and irreplaceability. The NFT has been very successful in proving the scarcity of the work. Thereby creating value and demand for collectors, artists, and trading parties.

Many high-value collections have appeared since 2021. The most well-known are Bored Ape Yacht Club and Azuki. The two collections have attracted a large amount of value in a short period of time by developing a core product, creating an ecosystem around it, and focusing on community growth.

Along with many perennial collections such as CryptoPunks, The Sandbox, and Decentraland, Bored Ape Yacht Club and Azuki are among the top ten collections with the highest trading volume ever.

The top NFTs on OpenSea, ranked by volume, floor price and other statistics - Source: OpenSea

Previously, Ethereum held the majority of the most valuable collectibles. However, NFT on Solana is attracting more cash flow, and many high-value collections are appearing. Solana names appeared among the top NFT collections with the highest transaction volume on OpenSea.

One of the fastest growing NFT markets is Solana. Over 14.8 million NFTs have been generated from Metaplex, Solana's primary infrastructure for NFT generation. The total value of traded NFTs exceeded $3.1 billion.

In short, Ethereum still retains control of the Collectibles market. This piece of cake, however, is attracting many other parties, and we can expect to see the quintessential NFT collectibles of each ecosystem in the future.

NFT Gaming

Gaming is the next major application for NFT. The success of Axie Infinity's "Play-to-earn" concept has attracted a large number of projects to compete in this space. NFT is used in a variety of ways in the game, including the creation of characters, items, and assets.

However, the current gaming projects are unable to balance the supply and demand of assets and tokens due to a lack of a sustainable economic model. Axie Infinity, the game that started the P2E trend and is the best FDV growth project, is a good example.

Axie's daily revenue has occasionally exceeded 16 million USD per day; currently, this figure only ranges between $3,000 and $5,000.

In short, it seems that no GameFi model has been successful and has the potential for growth sustainably, as in the traditional market. This may change in the future as projects gradually focus on game quality in order to attract more users and generate long-term revenue.

Chains with stable performance and low costs, as well as specific app chains for gaming, such as Ronin, BNB Chain, Solana, ImmutableX..., will be more appealing to users than Ethereum. Solana will be noticeable among these when a series of games is released in 2022.

NFT ecosystems and their internal categories

NFTs are gradually becoming a necessary component of any blockchain ecosystem. NFT, like DeFi, is made up of various categories that make it easier to trade and leverage assets. Lower layer puzzle pieces must be complete and liquid enough to allow the upper layer puzzle pieces to form.

NFT Marketplace analysis shows that most of the NFT trading volume is still on Ethereum. However, Solana recently emerged as a phenomenon with strong growth from Magic Eden. Looking at the NFT marketplace puzzle piece, we can get a preliminary understanding of the development situation of NFT in each ecosystem.

Given the higher categories in the pyramid above, it is still too soon for those to reach success. The reason for this is that the current level of liquidity, combined with underperforming infrastructure (lower/foundation layers), is insufficient to keep the above puzzles running smoothly.

Projections

- NFT is a potential market and will continue to be developed.

- However, due to the nature of using the blockchain token to calculate the price of NFT, users will be exposed to double profits in an uptrend (the token price increases as well as the number of tokens).

- In a downtrend, however, users will suffer double losses (decreasing token price and decreasing amount of tokens). Furthermore, because NFT has low liquidity, the investment risk is high, and it is not recommended to participate in a downtrend.

- The developed ecosystems will have their own unique and notable NFT collections.

- The gaming segment will develop in a more sustainable direction with stronger tokenomics design.

- The higher layers of ecosystems will struggle until their foundation can run smoothly and with sufficient liquidity.

Limitations and solutions of DAO

DAO is a decentralized autonomous organization. Unlike traditional organizations (like Facebook, Google...), By applying code-coded rules, they can operate independently without human intervention.

Overview of DAO in the first half of 2022

DAO is a very broad topic, they exist from blockchains, DeFi protocols adopting an on-chain governance model, to groups adopting on-chain voting and proposal mechanisms in many different fields. Therefore, we can see the diversity in the development branches of the DAO in the past time.

Governance is a standard use case for project tokens in DeFi alone; the larger the project, the more valuable this use case is. Decisions are proposed and voted on by the token holders of the top projects with the highest TVL. The DAO model has become a "must have" for the evolution of DeFi protocols.

The value that DAOs possess has enormous development potential because they are used in so many other industries, including social, service, …

Case studies from the DAO Guild's demise

Emerging from the Play To Earn craze, Guild Game projects have grown tremendously with the start of the Yield Guild Game. The idea of the Guild is to create a place to optimize assets and share profits for token holders. In other words, the project connects players with the game.

However, most Guild projects at the moment have lost most of their value. Yield Guild Game's YGG token lost 94.5% of its value from the top, Merit Circle's MC token lost 93.2% of its value, GuildFi's GF token also dropped 92.8%...

The DAO's present operating paradigm is inefficient, which is the fundamental justification. Everything is disorganized and unclearly split in the existing DAO (now known as DAO 1.0), and it is unable to generate favorable development impacts (Positive feedback loop).

In the future or DAO 2.0 everything will be arranged and support each other. Everything works seamlessly together like a traditional corporate model but has great scalability as anyone participating will have the right to contribute to the DAO.

The future DAO will have a framework to be able to allocate resources, share revenue appropriately, and not create conflicts within the organization. At the same time, the limitations of the DAO above will also be gradually resolved.

Projection

DAOs are an important part of achieving decentralization (blockchain’s nature) and will continue to grow in the future.

Existing DAO problems will be solved with the right tools and infrastructure. This is also a potential branch for investment.

Conclusion

In the current context of the financial markets, the crypto market experienced a significant decline in the first half of 2022. While the negative macroeconomic effects will not abate anytime soon, the influence and associated risks of large crypto institutions' "domino fall" phenomenon have not been fully explored and exposed. It is possible that a bear market will emerge in the second half of 2022.

Also available in

Vie